Business Management | Hearing Review July 2014

Turning industry benchmarks into action points for your practice

By Ronald Gleitman, PhD

Why do we do benchmark studies? For practice owners and managers, the data is commonly used as a point of reference, allowing them to compare their own performance against those who responded. The information provides a visual snapshot of where they are in relationship to their peers and a glimpse into where they would like to be in the future. The data helps provide a vision—a mental plan of action for success.

However, as author Joel Barker points out, “Vision without action is just a dream.” Action, therefore, is the goal.

This paper discusses how to turn information from a practice benchmark study into action—to help hearing practice owners differentiate themselves from the competition.

Background and Key Findings

In September 2013, Siemens commissioned American Opinion Research (AOR) to repeat the benchmark study conducted 1 year prior (see August 2013 Hearing Review).1 The results reflect information gathered from the sample for the year 2012, as well as the first 6 months of 2013.

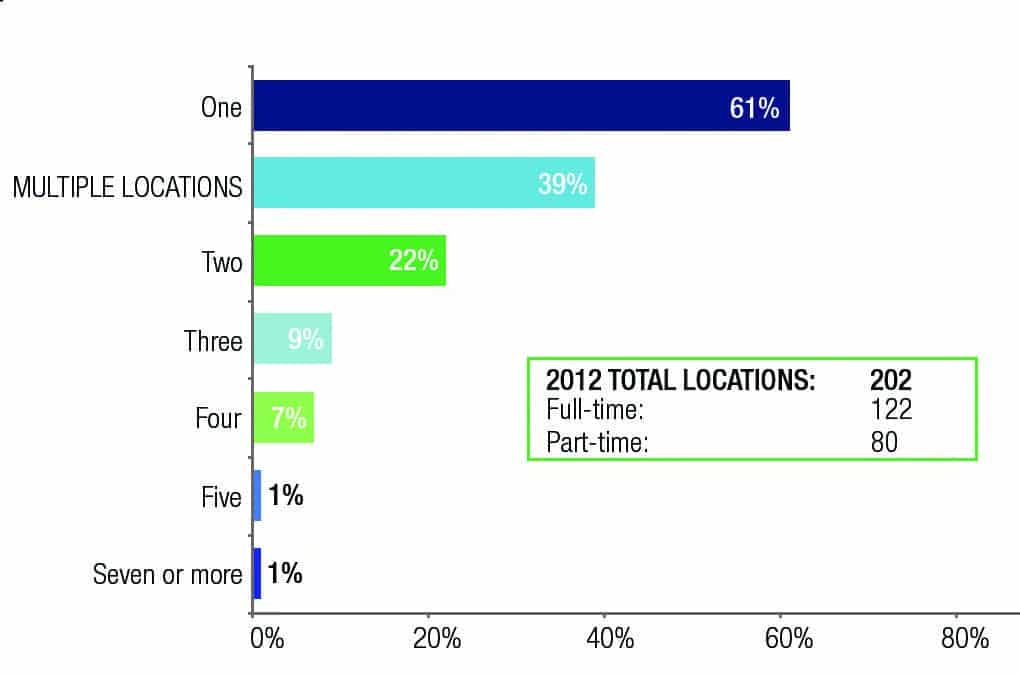

[Click on figure to enlarge.] Figure 1a. Number of locations

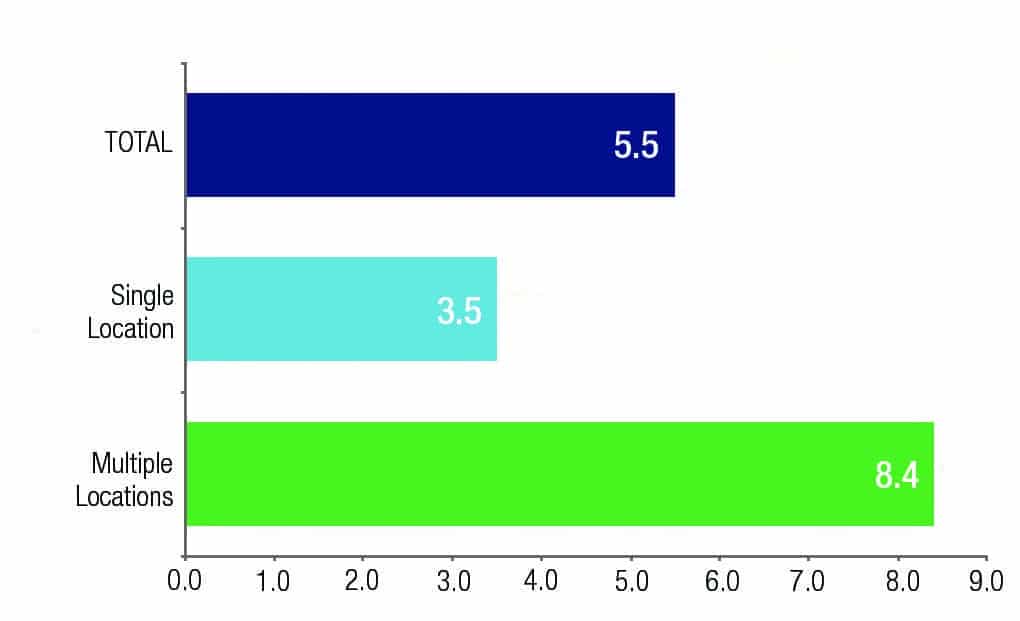

Figure 1b. The average number of hearing care professionals in single and multiple practices.

Demographics. The results of the study reflect today’s typical hearing aid practice. In fact, nearly 70% of all respondents were independent hearing care professionals (HCPs), mostly small to mid-size in staff size and number of locations (Figures 1a-b). Almost three-quarters of respondents (73%) identified themselves as an owner of the practice.

Financial/revenue. Compared to 1 year prior, the 2013 respondents averaged a decrease in Average Selling Price (ASP) for the year 2012, consistent with findings from previous benchmark studies.2 Lower ASPs could be a result of increased competition and/or because respondents did not separate out third-party revenue streams. For example, third-party payors have unbundled dispensing fees whereas traditional dispensing fees often include cost of goods sold (COGS), professional fees, and profit.

Compared to 2011, total average gross revenue and unit sales were lower in 2012. Total unit sales for the first half of 2013 were also down compared to the same period 1 year prior. These findings are consistent with data presented by the Hearing Industries Association (HIA).3 However, many practices did report increases in ASPs, revenue, and unit sales for the first half of 2013. HIA4 reports the industry is experiencing a year-over-year (YOY) growth rate of 4% to 5%.

People are certainly buying hearing aids. The question is to whom (or perhaps more appropriately where) are all the patients going?

One theory is that more patients are “purchasing” their hearing aids online, promoted by these companies’ lead generation programs. Another theory is that national retail (Big Box retailers) are invading the market. From 2009 to 2013, Costco’s hearing aid revenue grew on average 26%,5 while during the same period, Sam’s Club also increased its number of stores that sell hearing aids.

Business and patient care. As was the case in 2011, patient referrals remain the most common source of new patients, followed by physician referrals. Fewer than half of all practices follow up with patients on a quarterly or semiannual basis; 41% don’t follow up at all.

More than half (52%) of those who responded see and manage tinnitus patients, meaning almost half do not. Practices that have a formal tinnitus rehabilitation program report the program yields an average of 6% of their total business.

Figure 2. Marketing expenditures for practices for 2012.

Marketing expenditures. Marketing spend among all practices in 2012 is varied, with 23% spending less than $5,000 and 13% spending between $50,000 and $300,000 (Figure 2). The bulk of marketing dollars is spent on printed materials, and almost 60% don’t perform Internet or social media advertising. About 6 in 10 practices evaluate their marketing efforts and most respondents (76%) do not know their marketing cost per appointment.

Let’s now focus on how to turn this information into action with a focus on three core areas—Revenue/Financials, Patient Care, and Marketing. We’ll also examine the importance of differentiation in each of these areas to stay ahead of the competition.

I. Revenue/Financials

Gaining new business. To increase revenue, practices must have a robust strategy in place to stave off the competition and attract new patients. If we look at our study results, we see that on average new hearing instrument wearers made up 46% of total gross revenue. This number is markedly lower than the previous year (67%). So despite all the great technology packed into today’s hearing instruments, we’re still not improving our new patient penetration rate!

To compete (and win) in today’s market, practice owners should set a goal to have new patients make up at least 60% of total gross revenue. Practices can achieve this by developing their bundling/unbundling strategy and maximizing referral programs.

To bundle or not to bundle? Put simply, practices need to do both. The growing number of third-party payors into the hearing care industry already requires a strategy for unbundling. Those against unbundling should consider this: if they are already taking third-party referrals (eg, Hearing Planet or AARP), they are by nature unbundling.

To grow a practice, practice owners need multiple revenue sources with different service-pricing policies for various buying segments. They can start out by segmenting customers based on referral sources, then develop a strategy for different payors, taking into account the level of technology sold.

By providing payment options, they are providing value to the end user, which can lead to more profit over the course of the hearing instruments’ lifespan.

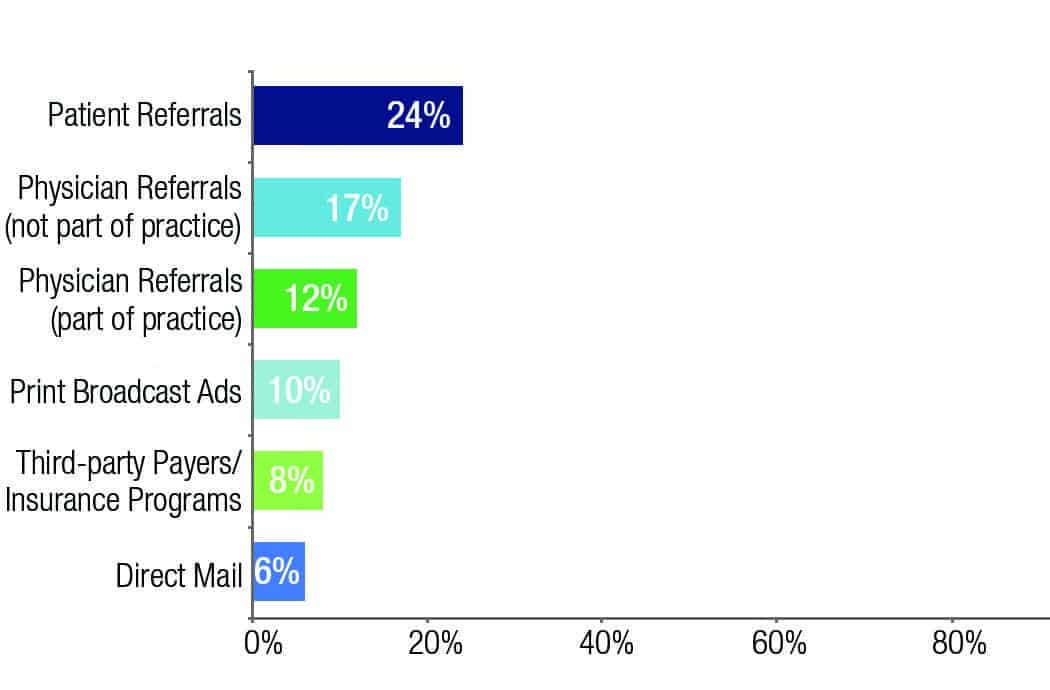

Figure 3. Source of patient referrals.

Referral programs. Referral programs are a simple way to attract new business while positioning a practice as the go-to provider in its market. Our benchmark study revealed that patient referrals are the most common source of new patients (24%), followed by physician referrals (17%, Figure 3). This shows us the continued power of word-of-mouth (WOM) advertising while demonstrating the need to actively engage referral sources.

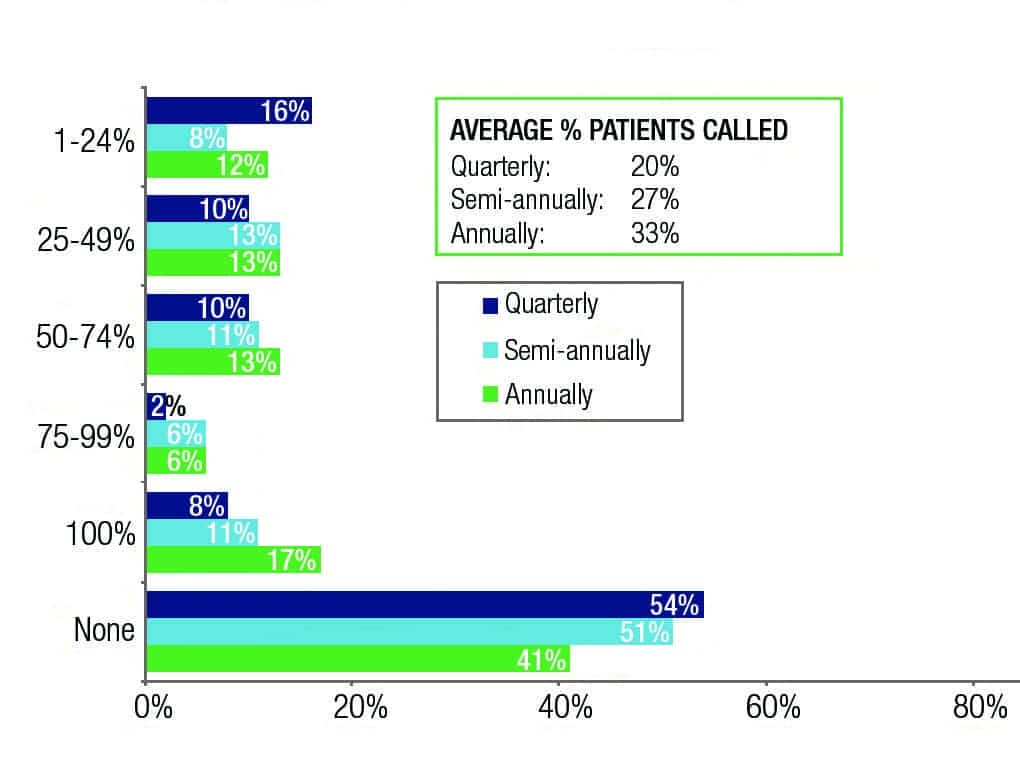

How do practices nourish these referral sources? They should start with the existing patient base first. Practice owners need to ask, “Am I providing a personalized experience that will make them want to tell others? Am I educating them in the latest diseases and comorbidities associated with untreated hearing loss?” They need to have a plan in place to follow up with patients on a regular basis. More than 40% of respondents indicated they perform zero follow-up with customers after the fitting (Figure 4). These are missed opportunities!

Figure 4. Percentage of patients called after the initial fitting.

Next, practice owners need to focus on physicians. Whether an independent dispensing practice or a medically based practice, physicians represent an opportunity for additional referrals. In fact, roughly 15% of physicians have incorporated hearing screenings as part of their normal practice’s adult evaluations.6

Practices need to make it a point to learn the facts about the Affordable Care Act (ACA) and how it affects hearing screenings for Medicare recipients. They should educate physicians in their area on the new research on hearing loss and diabetes, falls, cardiovascular disease, cognitive decline, and other disease states (see Taylor and Tysoe on page 22). By establishing an ongoing dialogue, practice owners can position themselves as trusted resources and partners while helping physicians preserve their own patients’ health and safety.

II. Patient Care

Another way to differentiate a practice is to provide a unique environment, unlike anything the competition can offer, complete with outstanding patient care. It’s a recipe for success with several key ingredients. These include: specialty products, expert services, and patient counseling.

Specialty products. Patients still cannot get ear impressions taken online. So, if the reason a practice only sells RICs is because fitting custom instruments is “a hassle,” then their product offering is not much different than the store down the street.

Respondents indicated the vast majority (60%) of instruments sold were RICs. There’s nothing wrong with selling RICs, but to stay competitive, in-the-ear (ITE) instruments should make up at least 20% of product offerings. Invisible hearing instruments—tiny completely-in-canals (CICs) with wireless connectivity—and even custom hearing protection are game changers in themselves.

Today’s consumers want options, so why shouldn’t HCPs give them more of what they want?

Expert services. Diagnostic services and tinnitus treatment are points of differentiation that also may result in additional revenue streams. While not every hearing care practice is qualified to perform a full range of diagnostic services, it’s important they advise patients on the services they can provide, from testing and fitting to verification and follow-up. They should consider providing services as both a bundled package and a la carte, depending on the payor and performance level of the instrument.

What about tinnitus treatment? Only half of our benchmark study participants see or manage tinnitus patients, while those with a formal tinnitus program have extremely low penetration rates (6%). Tinnitus is a very hot topic and is treatable with proper training and amplification. Yet, many are reluctant to include tinnitus treatment as part of their services, despite tinnitus therapy being available in so many instruments.7 Practice owners need to familiarize themselves with hearing instruments that have built-in tinnitus therapy treatment. By positioning themselves as tinnitus specialists, they’re providing a service that differentiates them from the competition.

Patient counseling. Price is not everything to everyone. If this wasn’t the case, then high-end shopping outlets and boutique businesses would no longer exist. Many buyers are happy to spend a little more to receive that personalized attention.

That’s where patient counseling techniques come into play. Practice owners need to focus on the patient experience (see Kasewurm on page 18). Are patients receiving a modern, robust counseling tool to actively engage them in the decision-making process? Are they being educated on comorbidities, the latest wireless accessories, and how to use their t-coils? What about an aural rehabilitation program, which has been associated with long-term acceptance and lower return rates?8 These are the conversations HCPs need to be having with patients. It helps them build a better relationship, increases their chances for referrals, and will lead to more satisfied patients who are “customers” for life.

III. Marketing

With all of today’s competition, marketing is no longer an optional activity. More than ever, the question is rather how to market which channels, and to whom. The truth is they don’t need to hire a full-time marketing manager to do marketing. But they do need some basic tools—specifically, a budget, a plan, and a modern strategy.

Budget, Plan…and Measure. According to our benchmark study, 57% of respondents do not budget funds for marketing. Out of the roughly 40% who do budget marketing dollars, less than 30% of them (29%) have an actual plan in place.

Practice owners should take one day out of the year to put together a simple marketing plan worksheet, decide how much to allocate to marketing, create a plan for the year, and schedule time every quarter to review marketing efforts to measure their effectiveness.

Take inventory of target audiences and develop a plan consisting of multiple channels to reach those targets most effectively. Consistent planning and implementation achieves results.

A Modern Strategy

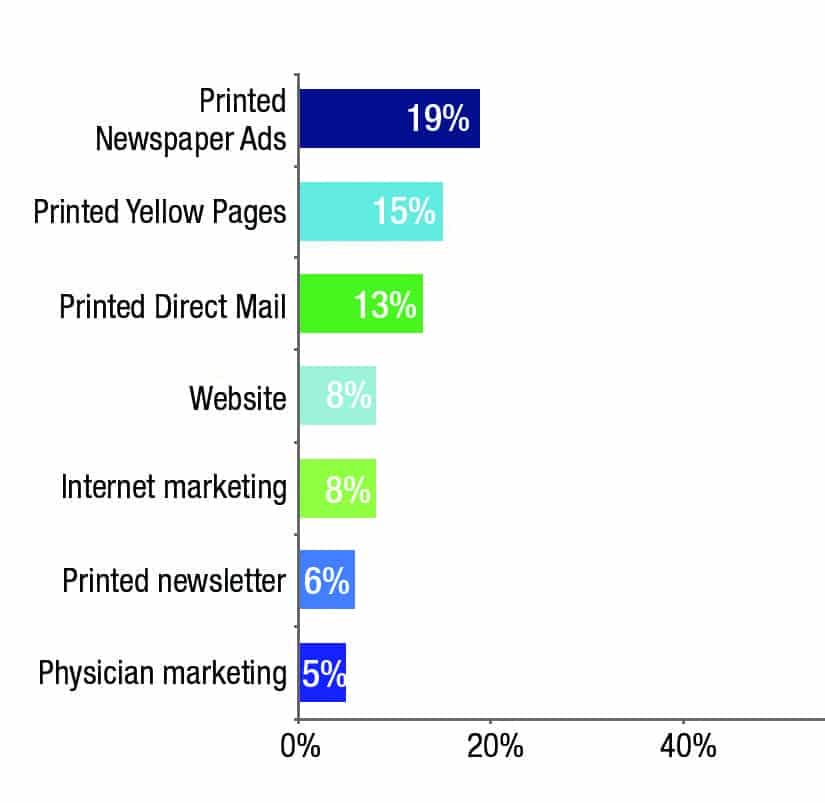

Figure 5. Marketing spend for dispensing practices as a percentage of their marketing budgets.

Our data showed that practices spread their marketing spend over a wide variety of vehicles, led by printed newspaper ads, followed by printed Yellow Pages and printed direct mail (Figure 5). Just as in 2011, an average of 60% did no Internet advertising.

As the market changes, so must a practice’s marketing strategy. Market pressures and changing dynamics demand new tactics. There is certainly still a place for traditional advertising vehicles like print newspapers and direct mailers. But to compete in today’s market requires more diversification to the digital realm.

A modern marketing strategy includes multiple referral sources. Practices should consider augmenting tactics by focusing on the people they want to get in front of. Physician and disease-state marketing is crucial. As Taylor and Tysoe point out, practices need to “educate to obligate” physicians.9

Disease-state and comorbidity marketing also needs to be in front of patients. An office should contain posters, infographics, and other collateral that tell patients you care about their overall well-being. It’s a quick and easy way to distinguish your practice from the others, giving credence to the personalized service that cannot be found elsewhere.

Digital marketing deserves a larger piece of the marketing pie. If HCPs think seniors are not using the Internet, they need to think again. A Pew Research study10 revealed that nearly 55% of people age 65+ use the Internet every day—and that number is growing steadily.

Practices need to be sure to incorporate search engine optimization (SEO) and search engine marketing (SEM) tactics like pay-per-click (PPC) into their marketing strategy. For example, adding a practice listing on Google Places is a quick and free way to get found easily. An online presence and outreach can define success—so practice owners need to invest in it wisely.

Differentiating Your Practice

Not too long ago, purchasing a hearing aid simply meant a visit to a local hearing care professional. The biggest competition may have been another local privately owned practice.

Fast-forward to today. New healthcare provisions, insurance companies, retail outlets, Big Box stores, and a growing online marketplace all present real and formidable competition. This should come as no surprise. In our survey, respondents easily ranked these highest among concerns over the next 3 years.

Yes, times are certainly changing. But as they change, so must the way HCPs do business. If HCPs want to stay competitive and relevant, and attract new patients, they need to level the playing field. One of the most effective ways to do this is through differentiation—regardless of which manufacturer they choose to do business with. Practices need to stop focusing solely on how they’re going to compete on price and instead compete on value and service—and on marketing (once they have a budget and plan in place)!

It’s a great time for HCPs to be CEOs of their businesses. The most successful CEOs know change is inevitable. They don’t fight it—they embrace it. To compete and win, practice owners must develop a strategy and execute their plans!

References

1. Gleitman R. Examination of the AOR benchmark practice management study. Hearing Review. 2014;20(8):26-31. Available at: https://hearingreview.com/2013/07/examination-of-the-aor-benchmark-practice-management-study-2

2. Strom KE. HR 2013 dispenser survey: dispensing in the age of internet and big box retailers. Hearing Review. 2014;21(4):22-28.

3. Strom KE. US hearing aid sales flat in first quarter of 2014. Hearing Review. 2014;21(5):6. Available at: https://hearingreview.com/2014/05/staff-standoff-us-hearing-aid-sales-flat-first-quarter-2014/

4. Hearing Industries Association (HIA). HIA statistical reporting program: Fourth quarter 2013. Washington, DC: HIA; 2014.

5. Stock, K. Why Costco rules in hearing aids…and gummy bears. Bloomberg Businessweek. http://www.businessweek.com/articles/2013-07-11/why-costco-rules-in-hearing-aids-dot-as-well-as-gummie-bears

6. Kochkin S. MarkeTrak VIII: 25-year trends in the hearing health market. Hearing Review. 2009;16(11):12-31. Available at: https://hearingreview.com/2009/10/marketrak-viii-25-year-trends-in-the-hearing-health-market

7. Kochkin S, Tyler R. Tinnitus treatment and the effectiveness of hearing aids: hearing care professional perceptions. Hearing Review. 2008;15(13):14-18.

8. Martin M. Software-based auditory training program found to reduce hearing aid return rate. Hear Jour. 2007;60(8):32-35.

9. Taylor B, Tysoe B. Interventional audiology: partnering with physicians to deliver integrative and preventive hearing care. Hearing Review. 2013;20(12):16-22.

10. Pew Research. Pew Internet Health Fact Sheet. Available at: http://www.pewinternet.org/fact-sheets/health-fact-sheet

Original citation for this article: Gleitman R. How data from a practice benchmark study can help hearing practices compete—and win: Turning industry benchmarks into action points for your practice. Hearing Review. 2014;21(7):14-17.

Original citation for this article: Gleitman R. How data from a practice benchmark study can help hearing practices compete—and win: Turning industry benchmarks into action points for your practice. Hearing Review. 2014;21(7):14-17.