By Karl Strom, editor-in-chief

Premium products are back. With a few notable exceptions, the last 2 to 3 years have been marked by

less sexy and more prudent mid- to low-end hearing aid product launches. Although much of this has to do with R&D timing and subsequent product life-cycles, these lower-end product introductions have also coincided with the most severe recession in living memory. Economically speaking, it was fortunate and beneficial for manufacturers to concentrate on more affordable hearing solutions during this period. And, as pointed out in previous editorials (eg, March 2008 Staff Standpoint, “Are We Recession Proof?”), the hearing industry is uniquely positioned (compared to other industries) to withstand the worst effects of recession. Focusing on more economical products for consumers was a no-brainer.

However, premium hearing aid launches took center stage at the EUHA 2012 Congress held in Frankfurt, Germany, this October. Several hearing aid manufacturers introduced or announced premium product lines, including ReSound (Verso, see p 26), Siemens (micon, see p 32), Phonak (Quest), Unitron (Flex), Hansaton (AQ 2G), and others. Likewise, more premium products are scheduled for introduction in early 2013 and beyond.

|

|

|

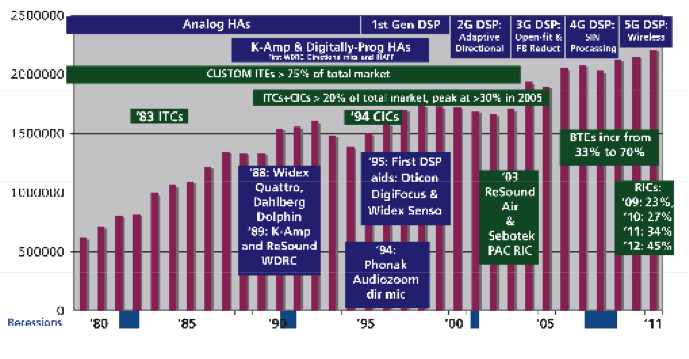

(Click to enlarge) Figure 1. A rough schematic of hearing aid technologies (blue) and styles (green) during the last 30 years, as well as unit volume (magenta). |

I’ve presented in Figure 1 an admittedly rough schematic of hearing aid and integrated circuit (IC) technology development (in blue), as well as styles/form factors (in green), since 1980. The figure also shows net unit hearing aid volume in magenta, as reported by the Hearing Industries Association (HIA). It should be pointed out that many hearing aid manufacturers are well beyond their 5th generation (5G) of ICs; for example, Thomas Powers, PhD, reports on p 32 that Siemens is now on its 8th generation. However, in terms of major technological innovations, I tend to think of the progression of digital signal processing (DSP) aids as:

1G: The first commercial implementation of DSP replicating the previous analog digital programmable aids with some important enhancements and refinements;

2G: The first breakthrough uses of adaptive directional systems;

3G: Open-fit and advanced feedback and occlusion reduction systems;

4G: Speech-in-noise processing that provided for better comfort and reduced cognitive processing load in difficult listening environments;

5G: True wireless capabilities, both via inter-ear and to external mics/receivers.

This brings us to 6G. Currently, it would appear that the new generation of digital aids provide new wireless capabilities, directional processing strategies, tinnitus relief solutions, frequency-lowering for severe hearing losses, music processing strategies, and abundant options (eg, 2.4 GHz) for interacting with telephones and TVs—a kind of smorgasbord of solutions to some of the thorniest problems facing hearing-impaired consumers, as detailed in MarkeTrak VIII (February 2012 HR). And more is on the horizon. As this month’s cover of HR suggests, let the races begin!