|

| Sergei Kochkin, PhD, is executive director of the Better Hearing Institute, Washington, DC. |

Research | October 2009 Hearing Review

This is the first segment of a multi-part publication that will cover significant trends and issues in the hearing loss population. Since 1989, Knowles Electronics has conducted six MarkeTrak surveys of the US hearing loss population following the landmark 1984 Hearing Industries Association (HIA) study. Starting in 2004, the MarkeTrak national study was conducted and published by the Better Hearing Institute (BHI) through the continued generosity and sponsorship of Knowles Electronics as a public service to the hearing care industry.

As in the past, the goal of this survey is to report relevant trends and report on new topics that contribute to our knowledge of the hearing aid owner population, as well as the sizeable population of people with admitted hearing loss who have chosen not to adopt amplification for their hearing loss. This publication covers 25-year trends in the hearing-impaired population including:

- Hearing loss prevalence,

- Hearing aid adoption rates,

- Hearing loss screenings during a physical exam,

- Distribution of hearing aids,

- Hearing loss characteristics of hearing aid owners and non-adopters,

- New hearing aid adopters, and

- Demography of hearing aid owners and non-adopters.

Two key changes to the trending publication are: 1) overall customer satisfaction trends have been removed from this report; and 2) comparisons of hearing loss characteristics of hearing aid owners and non-owners have been moved from the traditional survey of non-adopters to this trend and demography publication (see “More on Trak” for future MarkeTrak VIII publications at the bottom of the page).

|

| FIGURE 1. Prevalence of hearing loss per 1000 households. |

|

| FIGURE 2. Looking back at the percent of the US population reporting hearing loss (1989-2008) in MarkeTrak versus the 1984 HIA survey. |

Survey Method

In November and December 2008, a short screening survey was mailed to 80,000 members of the National Family Opinion (NFO) panel. The NFO panel consists of households that are balanced to the latest US census information with respect to market size, age of household, size of household, and income within each of the nine census regions, as well as by family versus non-family households, state (with the exception of Hawaii and Alaska), and the nation’s top-25 metropolitan statistical areas.

The screening survey was expanded from previous screeners to include:

- Physician/staff screened for hearing loss during their physical in the last year;

- Whether the household had one or more people “with a hearing difficulty in one or both ears (without hearing aid)”;

- Whether the household had one or more people who were the owner of a hearing aid;

- Whether the household had one or more people with tinnitus (ringing in the ears);

- Perceptions of job discrimination in promotions/salary equity;

- Detailed quantification of employment status (beyond simpler NFO panel data); and

- Traffic accidents over the past 5 years and driving habits.

This short screening survey was completed by 46,843 households and helped identify 14,623 people with hearing loss and also provided detailed demographics on those individuals and their households. The response rate to the screening survey was 59%. In January 2009 an extensive 7-page legal-size survey was sent to the total universe of hearing aid owners in the panel database (3,789); 3,174 completed surveys were returned representing an 84% response rate. In February 2009 an extensive 7-page survey was sent to a random sample of 5,500 people with hearing loss who had not yet adopted hearing aids. The response rate for the non-adopter survey was 79%. Both hearing aid owners and non-adopters were given a $1 incentive to complete and return their surveys.

The data presented in this article refer only to households as defined by the US Bureau of the Census, ie, people living in a single-family home, duplex, apartment, condominium, mobile home, etc. People living in institutions have not been surveyed; these would include residents of nursing homes, retirement homes, mental hospitals, prisons, college dormitories, and the military. The reader should also keep in mind that the demographics presented here refer only to those who are aware of, and admit to, their hearing loss.

Results and Discussion

Data presented in this study compare the MarkeTrak survey results over the last 20 years with selected data from the 1984 Hearing Industries Association (HIA) database of the hearing loss population. Tables 1 to 7 contain general trends and indices of the hearing loss and hearing aid owner populations. Each table will be discussed in the order of appearance with references to relevant figures. (Note: Sample sizes are denoted in each table by “n =”.)

Hearing Loss Population

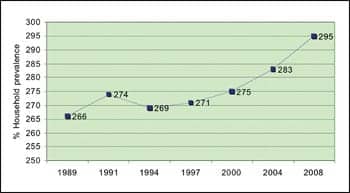

As measured by MarkeTrak, the incidence of hearing loss per 1,000 households increased to 295 from 283 in 2004. When we consider that the incidence of hearing loss was 266 in 1989, we can discern a steady increase in hearing loss prevalence as shown in Figure 1.

|

| FIGURE 3. Hearing aid adoption rates expressed as a percent of people with admitted hearing loss who own hearing aids. |

|

| FIGURE 4. Binaural hearing aid adoption rates (%). |

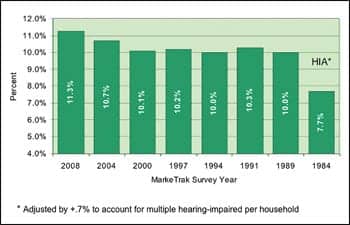

In 2008, the hearing loss population increased to 34.25 million people reporting a hearing difficulty. Since 2004, the hearing loss population grew 8.8% compared to a 4.5% increase in US households. In addition, the percent of the US population reporting hearing loss in the last generation increased from 10% in 1989 to 11.3% in 2008 (Figure 2). The Hearing Industries Association (HIA) survey (1984 data point in this study) reported a 7.7% incidence of hearing loss using similar methodology as MarkeTrak.1 A survey of 1,600 adults by the Gallup Organization on behalf of the HIA in 1980 reported a 9% incidence of hearing loss.2 Self-report studies by the Centers for Disease Control in 1971 and 1977—from which MarkeTrak is modeled—reported a 7% incidence growing to 8.6% in 1990.3

Is there evidence of a hearing loss “epidemic” when we look at MarkeTrak trends and consider the results of the National Health and Nutrition Examination Survey (1999-2004) published in the Archives of Internal Medicine4 in 2008? When the NHANES study was released, the press around the world proclaimed that the study demonstrated a possible hearing loss epidemic in America.5 The authors of this study estimated that 16.1% of US adults ages 20-69 (29 million people) had speech frequency hearing loss of at least 25 dBHL and that 31% (55 million people) had high frequency hearing loss of at least 25 dBHL. The NHANES study demonstrated approximately a 1% point increase in the prevalence of hearing loss between the 1999-2000 and 2003-2004 studies and a 1% decline in high frequency hearing loss. Dr Yuri Agrawal, the principal author, stated:

“The prevalence of hearing loss in the United States is predicted to rise significantly because of an aging population and the growing use of personal listening devices. Indeed, there is concern that we may be facing an epidemic of hearing impairment.”4

When you consider that the NHANES study did not include the ages 70+ population, then the number of people with measurable hearing loss is even more staggering. In fact, in our MarkeTrak self-report study, we are estimating at least 12.5 million adults ages 70 years or higher with self-report hearing loss—and our figures only include people living in non-institutional settings.

The incongruities between self-report and objective studies of the pediatric population are even greater. Based on self-reports from parents, only slightly more than a million children have hearing loss (see Table 5). Yet objective data from the third NHANES (1999-2004)6 estimated that 14.9% of children ages 6 to 19 years (more than 7 million children) have at least a 16 dBHL low or high frequency hearing loss in one or both ears; the majority of the hearing loss was unilateral and classified in the “slight” hearing loss range (16-25 dBHL).

I believe we can make several conclusions from these studies. There is some evidence that hearing loss is increasing in prevalence in America as evidenced by MarkeTrak (which is modeled after the CDC survey methodology). However, over the last generation, the incidence has for all practical purposes been steady at 1 in 10 Americans reporting a hearing loss.

The objective studies report higher incidence for both adults and children using a 25 dBHL and 16 dBHL cut-off, respectively. However, in the pediatric population, the majority of the children have a slight hearing loss. The differences in objective and subjective measured hearing loss populations are perhaps due to the following:

- There is no universal hearing loss screening program for children or adults in America. As shown in this study, the historical incidence of physician screening for hearing loss has been low. One would expect a slight-to-normal hearing loss to go undetected or to be nearly imperceptible to the adult or parent of the child, even though in the case of children even a mild hearing loss could impact school performance.

- The cut-offs used in the objective studies are considered in the normal range for adults and in the slight-to-normal hearing loss range for children. So there may be some confusion on the part of the general population (eg, a slight or very mild hearing loss could be classified as in the normal range), and thus the survey respondent subjectively perceives that they do not have a hearing loss.

- Some people reporting lack of hearing loss may consciously or subconsciously deny or minimize their hearing loss.

- Some people do not consider their hearing loss a “real” hearing loss unless they are aware that the loss has an impact on their everyday functioning.

- Some people may not consider themselves as having a hearing loss if they have a mild high frequency hearing loss and normal hearing in the speech range.

In conclusion, there is evidence of a minor increase in prevalence in hearing loss over the last quarter century. According to self-report surveys, slightly more than 1 in 10 Americans are aware of and report they have a hearing loss. Studies using objective measures with low dBHL cut-offs report significantly higher incidences of hearing loss in the American population. For children, the estimates of hearing loss are 7 to 8 times higher than data reported by their parents, and for adults at least double or triple self-report measures in MarkeTrak.

Considering the population measured—as well as the population not measured (ages 70-plus)—by the objective national surveys, one could make the argument that close to 100 million Americans have some form of hearing loss. What remains unanswered is how many people have a practical hearing loss that interferes with their ability to function optimally in a hearing society, making them candidates for treatment.

|

| TABLE 1. Some general characteristics of the hearing loss population, including number of households having a person(s) with hearing impairment, percentage of hearing aid users, user vs non-user data, hearing aid devices owned and in use, binaural utilization, and hearing screening data. |

The Hearing Aid Population

Referring to Figure 3 and Table 1, hearing aid adoption rates declined steadily between 1984 and 1997. Starting in 2000, the hearing aid adoption rate rebounded and increased to 24.6% in 2008—its highest since we began measuring adoption rates. Historically in industry press releases it has been stated that only 1 in 5 people with a hearing loss use hearing aids; this has now grown to 1 in 4. However, it should be understood that hearing aid adoption is intimately related to degree of hearing loss, lifestyle, need, as well as many other moderating variables.7 Yet, it would seem that even this statement, while technically correct, is probably practically incorrect. Later in this paper I will propose another method of reporting US hearing aid adoption rates based on multiple measures of hearing loss.

Figure 4 shows the historical growth rate for binaural hearing aid purchases. Since our last survey in 2004, the binaural population increased from 69.6% to 74.3% for all users, and from 82.3% to 86% (Table 1) for all bilateral loss consumers. The binaural purchase rate in 2008 increased to 78.8% for all users and 89.8% for bilateral loss consumers.

Physician Screening for Hearing Loss

We specifically asked individuals who received a physical exam in the last year to indicate if their physician or nurse screened for hearing loss during that exam (Table 1). Previous surveys asked if the physician or staff screened for hearing loss in the previous 6 months. Starting in the 2008 survey, we defined hearing screening to include electronic screening, paper and pencil test, tuning fork, or whisper test. The historical trends are shown in Figure 5. Reported physician screening increased to 14.6% for the total population.

Defining what we meant by hearing screening increased the reported incidence of hearing screening for all age groups. It is encouraging that 40.6% of individuals ages 45 to 64 report they received some form of screening and that 29.1% of adults ages 20 to 44 reported receiving a screening.

However, the elderly (ages 65-plus) report only a small increase in hearing screenings. This is particularly perplexing given the fact that the Medicare Prescription Drug, Improvement and Modernization Act of 2003 encouraged the use of screening questionnaires to determine if patients have hearing or dizziness problems. The NIH endorsed the Hearing Handicap Inventory for the Elderly (HHIE) as a screening tool. If the patient does not pass the HHIE, the physician must provide education, counseling, and referral.

|

| FIGURE 5. Physician screening for hearing loss during last physical exam. |

Hearing Loss Demography

Since hearing aid adoption is related to degree of hearing loss, both aided and unaided subjects were asked to complete the following subjective measures of hearing loss. They were then segmented into 1 of 10 groups (called deciles) based on their responses to five measures of hearing loss:

- Number of ears impaired (ie, 1 or 2 ears);

- Score on the Gallaudet Scale.8 This 8-point scale indicates whether they can understand speech under several conditions (eg, “whisper across a quiet room,” “loud speech spoken into their better ear,” “not able to understand loud speech in their better ear,” “tell noises from each other,” “hear loud noises at all,” etc). An individual’s score ranges from 1 to 8 and is typically classified into one of 5 groups (1-hear whisper, 2-hear normal voice, 3-hear shouts, 4-hear speech in loud ear, 5-can’t hear speech). What makes the Gallaudet Scale of particular value is it has been validated against clinical information (dB loss in better ear). The Gallaudet Scale has historically been used by the Centers for Disease Control and Prevention in their quantification of the hearing-impaired population.

- Subjective hearing loss score. The respondent subjectively evaluated their hearing loss as “mild,” “moderate,” “severe,” or “profound.” This measure is given a score of 1 (mild) to 4 (profound).

- Difficulty hearing in noise. This 5-point scale runs from “extremely difficult” hearing in noise to “not at all difficult,” and is based on the work of Plomp.9

- BHI Quick Hearing Check. This 15-item 5-point Likert scaled hearing loss inventory is based on the revised American Academy of Otolaryngology-Head & Neck Surgery (AAO-HNS) Five-minute Hearing Test10 and has been shown to be correlated with objective measures of hearing loss.

|

| TABLE 2. Characteristics of hearing loss population (hearing aid owners versus non-adopters), with percentages of unilateral and bilateral losses, perceived magnitude of loss with various indices of severity, and number of years consumers have been aware of their hearing loss. |

A factor analysis of the above subjective measures was performed revealing a single subjective measure of hearing loss. Factor analysis is a method for extracting common variance among multiple variables. A composite hearing loss score was determined by computing factor scores for hearing aid owners and non-adopters. Based on their score, they were placed into one of 10 hearing loss groups where Decile 1 represented the mildest hearing loss (ie, the lower 10% of people with hearing loss) and Decile 10 represented the most serious hearing loss (ie, the top 10% of people with hearing loss). Finally the data was weighted to reflect hearing aid owners and non-adopters in the general population.

Table 2 documents the degree of hearing loss for 3,109 hearing aid owners and 4,209 non-adopters. Hearing aid owners are more likely to have a bilateral loss than non-owners (87% versus 61%), to have a perceived loss of severe to profound (40% versus 12%), to have more difficulty hearing normal speech across a room without visual cues (64% versus 34%), to have difficult hearing in noise (66% versus 34%, “quite difficult” to “extremely difficult”), and more likely to score in the top quartile (75th percentile) of the BHI Quick Check (45% versus 17%). The composite measure of hearing loss, broken down into deciles, demonstrates that 83% of hearing aid owners are in the top 6 deciles (top 60% of people with hearing loss) compared to 43% for non-adopters.

|

| TABLE 3. General indices for the hearing aid market, including percentage of purchases involving third-party payments, average price to consumers, and distribution data relating to professionals dispensing hearing aids and the purchase location. |

Hearing aid adoption rates are also documented in Table 2 for each hearing loss measure, and Figure 6 shows the adoption rate by decile for the composite hearing loss measure. A logical cut-off for likelihood of hearing aid adoption would be Decile 5, since 83% of hearing aid owners can be found above this cut-point compared to only 43% of non-adopters.

Extrapolating from the non-adopter population in Table 1, 11.1 million non-adopters have hearing loss equal to or greater than the current hearing aid user population. So it is these people who represent the most likely “untapped” market for potential hearing aid users. Hearing aid adoption rates for people in the top-6 deciles are 38%, but only 9% for people in the bottom-4 deciles (lower 40% of hearing loss). Perhaps a more precise definition of hearing aid adoption in the United States is as follows: 4 out of 10 people with moderate to severe hearing losses and 1 out of 10 people with milder hearing losses adopt hearing aids to treat their hearing loss.

Finally, we asked hearing aid owners how many years they waited to adopt hearing aids after they learned they had a hearing loss. Non-adopters were asked how long they have been aware of their hearing loss. The mean (average), median, and modal responses are reported at the bottom of Table 2. The average for hearing aid owners is 6.7 years compared to 12.4 years for non-owners; a more accurate measure, considering the distribution of responses, is the median of 3 years for hearing aid owners and 8 years for non-adopters.

|

| FIGURE 6. Hearing aid adoption percentage rates for each hearing loss decile. The hearing loss decile is a hearing loss composite score, expressed in 10% points, based on the hearing loss population data in Table 2. A total of 83% of all hearing aid adopters in MarkeTrak VIII were in the six most severe hearing loss deciles (Deciles 5-10). |

|

| FIGURE 7. Trend of the percentage of purchases involving third-party payment, with and without the Department of Veterans Affairs (VA). |

|

| FIGURE 8. Sources of third-party payment achieved in 2008 (n=298). Average third-party payment discount achieved = 84%. |

|

| FIGURE 9. Average out-of-pocket retail price paid by consumers (includes free, direct mail hearing aids, and all third-party discounts but excludes VA fittings). |

Price of Hearing Aids

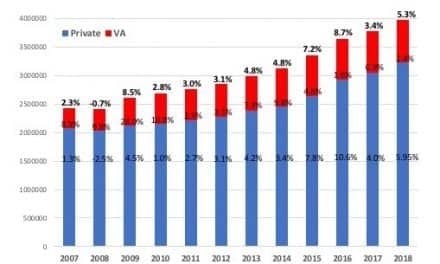

Referring to Table 3, third-party payment (eg, Medicare, union, insurance, HMO, VA, rebates, family members, etc) for hearing aids grew to nearly 4 in 10 hearing aids (39.7%) sold in 2008, up 2.4% points over 2004 (Figure 7). Excluding VA fittings, third-party payments in calendar year 2008 played a role in 30% of all hearing aid purchases, up nearly 8 percentage points from 2004.

In this survey, we asked individuals receiving any form of third-party payment to report the source. Referring to Figure 8, nearly 4 out of 10 (36.2%) third-party payments were through the VA, followed by insurance (23.2%), Medicare (17.1%), Medicaid (14.8%), and HMO (10.4%). Charity, union, and family help were less than 5% each. While we are aware that some children receive help through Medicaid, we were surprised to see the discount achieved through Medicare (traditionally Medicare does not reimburse hearing aids); it is possible that the payment for audiological testing was covered by Medicare, causing the consumer to believe they received a partial discount on their hearing aids.

The average price of a hearing aid as paid out of the consumer’s pocket (includes free and third-party discount excluding VA fittings) increased 16.9% to $1,601 (Figure 9). The price increases by style of hearing aid were: BTE (18.1%), ITC (-1.1%), ITE (5.2%).

Distribution

As shown in Table 3, the dispensing role of the audiologist rebounded from 2004 as perceived by the consumer of hearing aids to 62.9% (Figure 10). In comparison, hearing aid specialist fittings decreased 4.8% points to 31.1% of sales in 2008. Hearing aid fittings by medical doctors remain insignificant while direct mail fittings declined to 4.5% of sales, down from 7.1% in 2004. It should be understood that the distribution data represents perceptions of the consumer, who may not always be able to differentiate an audiologist from a hearing aid/instrument specialist.

Figure 11 shows that fittings in audiologist offices increased to 31.2% in 2008 from 24.9% in 2004 while fittings in hearing instrument specialist offices declined to 31.1% from 35.9%. VA fittings held steady at close to 1 in 7 hearing aids fitted in the United States, while fittings in ENT offices increased to 9.2%. Mail order sales decreased slightly to 4.7% (versus 5.4% in 2004). There were no significant trends in hearing aid fittings in wholesale clubs, retail stores, clinics and hospitals, etc.

The average age of hearing aids owned by consumers dropped to 4.1 years after a steady increase in age since 1991 (Figure 12). This is due to the fact that nearly half (47.9%) of hearing aids are less than or equal to 2 years of age, as customers with hearing aids 5 years old or more traded their old hearing aids in for newer technology such as open-fit.

|

| FIGURE 10. Hearing aid fittings dispensed by profession (% of fittings) as perceived by the consumer. |

|

| FIGURE 11. Hearing aid fittings by source of distribution as perceived by the consumer ranked in order of 2008 fittings. |

New Hearing Aid Owners

Referring to Table 4 and Figure 13, first-time hearing aid owners decreased in 2008 to 36.6% of fittings from 39.3% of fittings in 2004. The age of new users declined by about 1 year, but is still in the age 69 range (Figure 14) with an annual household income of $54,100 (Figure 15).

Factors influencing new first-time owners to purchase a hearing aid in 2008, while dropping in overall percent, remain remarkably constant in a relative sense (Table 4). The key factors influencing new users were: perception that their hearing loss was getting worse (55.4%), family members (51%), audiologists (26.4%), and ear doctors (18.2%), followed by receipt of free hearing aids (8.5%), hearing aid specialists (8.5%), and the recommendation of other hearing aid owners (7.4%). The family doctor, price of hearing aid, and safety concerns had minor influence, ranging from 6.8% to 5.1%. No aided-awareness advertising, marketing, or media influence garnered more than 5% of mentions.

|

| TABLE 4. New hearing aid owners: first-time hearing aid purchasers as a percentage of all purchasers of hearing aids, as well as their average age, income, and key reasons for purchase. |

Hearing-loss Population Demography

|

| FIGURE 12. Average age of hearing aids in the marketplace. |

|

| FIGURE 13. First-time hearing aid user rate expressed as a percent of hearing aid sales. |

Table 5 presents detailed demography for the year 2008, and hearing aid adoption rates are compared for selected years between 1984 and 2008. The most significant changes in hearing aid adoption rates during this time (emphasizing 1994-2008 due to low sample size in the 1984 HIA survey) were for children (7% points), but market penetration increased most significantly for individuals ages 85-plus (19% points). Penetration rates also increased approximately 6 percentage points for individuals earning $40,000-$49,000 per year, increased 7 percentage points for individuals holding post-graduate degrees, and increased 13 percentage points for young singles.

In the second part of Table 5, the demography is expressed as percentages for both the hearing aid owner and non-owner populations, while the third part of the table expresses the information in population size. To summarize:

- About 6 of 10 hearing aid owners and non-owners are male; this gender mix has held steady for the last 25 years.

- Non-adopters are significantly younger than hearing aid owners (Mean = 58 versus 70; Median = 60 versus 74).

- Non-adoptors, on average, are more affluent. Their average household income is $60,200 (median = $48,800) compared to $56,700 (median = $42,300) for hearing aid owners.

- Both non-adopters and hearing aid owners have similar educational profiles.

- 57% of adult non-owners are employed (part or full time) compared to 31% of adult hearing aid owners.

- The modal lifestyle of a hearing aid owner is “retired couple” (29%), while the modal lifestyle of a non-owner is “older parents” (24%). This is unchanged compared to 2004.

|

| TABLE 5. Hearing aid adoption rates and populations by selected demography. |

|

| TABLE 6. Changes in demographic segments of people with hearing loss. |

In Table 6, each of the demographic segments is compared over an 18-year period: MarkeTrak III (1991) versus MarkeTrak VIII (2008), and the percentage change is also shown. In the final column of Table 6, the hearing loss population is indexed to the US population (for example, a result of 1.5 means that the hearing loss population grew by one-and-a-half times, or 150%, compared to the US population). Key findings include:

|

| FIGURE 14. Average age of new hearing aid users. |

|

| FIGURE 15. Average household income of new hearing aid users. |

|

| FIGURE 16. Hearing aid opportunity by age group. Hearing loss Deciles 5-10 versus Deciles 1-4 comparing hearing aid owners and non-adopters. |

- The hearing loss population grew at 160% of US population growth rate.

- The female hearing loss population is growing slightly more than the male population (35% versus 31% for males).

- The population of hearing-impaired people ages 18-44 appears to be decreasing, while the age 85-plus hearing-impaired population is growing at nearly 12 times US population growth, and the age 75-84 population is growing at nearly 4 times population growth.

- Those with hearing loss and a household income of $60,000-plus increased at 10 times population growth. (As the United States population becomes more affluent, we will need to go back into previous surveys to expand income segmentation above $60,000.)

- With respect to the hearing loss population and education, the greatest increase was in achievement of some high school (11 times population growth) and achievement of a college degree (5 times population growth).

- People with hearing loss are less likely to be employed (70% of population growth), and more likely to be retired (160% of population growth) or employed part-time (150% of population growth).

- People with hearing loss are less likely to be living in small towns (-130%) and more likely to be living in large metropolitan areas (370%).

- Finally, in terms of lifestages of those individuals with hearing loss, the greatest increases have been in middle-age to older singles (300%-400%), working older couples (380%), and older parents. The most significant declines were in young to middle-age parents.

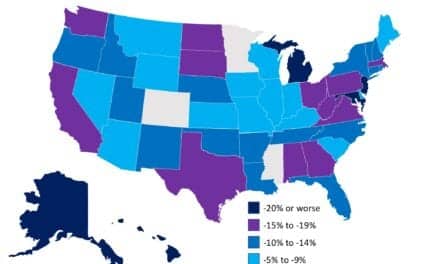

Table 7 shows data for state-by-state hearing loss population and incidence. The states with the highest incidence of hearing loss are Wyoming (18%); Arkansas, Missouri, and Montana (16%); and Kentucky (15%).

Toward More Meaningful Data Relative to Hearing Help

The data shown in this study suggests the hearing loss population is growing at 160% of the population growth and nearly 35 million Americans have a self-reported hearing loss. Objective scholarly studies indicate that perhaps three times as many people may have either speech or high frequency hearing loss. The logical question is how many of these people with hearing loss need help with their hearing?

There may be the assumption that everyone with some degree of hearing loss is a candidate for amplification, just like everyone with some degree of vision loss may be a candidate for eyeglasses or contact lenses. Some light on this question may be shed by Figure 16, where mild hearing loss (Deciles 1-4) and moderate-to-severe hearing loss (Deciles 5-10) have been segmented by age group (in thousands). The cut-point of hearing loss Decile 5+ in this study is that point where 83% of current hearing aid owners reside (refer to Figure 6). The key point in Figure 16 is that 11.1 million non-adopters have hearing loss equal to or greater than current users of amplification.

Notice that the population of non-adopters in Deciles 1-4 (those with low probability of use of amplification) exceeds that of non-adopters in Deciles 5-10 (those with the greatest need); people with mild hearing loss simply don’t use or perhaps need amplification for their hearing loss. In fact, only 9% have hearing aids. The largest opportunity to the hearing health care industry is in the ages 55 to 64 population (3.2 million people), followed by those ages 65 to 74 (2.3 million) and ages 45 to 54 (2.1 million).

|

| TABLE 7. State-by-state hearing loss by population and incidence. |

In summary, 11 million non-adopters belong in hearing care offices today to receive treatment for their hearing loss. The remaining 15 million non-adopters should continue to be educated on hearing loss, prevention, and treatment; in the next 10 years, many of them will move into the viable hearing aid candidate range.

In our previous MarkeTrak VII non-adopter study,7 we demonstrated that the issue of moving a person from admission of their hearing loss, to recognition of the problems hearing loss causes in their lives, to positive action to treat their hearing loss, is extremely complex and multi-dimensional. Early education to achieve recognition and positive perception change of non-adopters on the value of hearing health care remain priorities for the foreseeable future.

Key Findings

- The hearing loss population has grown to 34.25 million. Over the last generation, the hearing loss population grew at the rate of 160% (1.6 times) of US population growth, primarily due to the aging of America.

- Hearing aid adoption continues to increase slowly (now 1 in 4 people with hearing loss) as do binaural fittings (8 out of 10). However, less than 1 in 10 people with mild hearing loss use amplification, while 4 in 10 people with moderate-to-severe hearing loss use amplification for their hearing loss.

- Hearing screenings by physicians increased to 14.6%, possibly due to our adding “paper and pencil” test to our definition of a hearing screening. However, the gains were primarily in the younger segments.

- The first-time user profile is virtually unchanged, probably meaning that open-fit hearing aids did not tap any new market segments.

- There is evidence that the prevalence of hearing loss is increasing; however, neither the prevalence data nor demography changes support an argument that hearing loss is at “epidemic” proportions.

Acknowledgement

This study was made possible by a special grant from Knowles Electronics Inc, Itasca, Ill.

Correspondence can be addressed to The Hearing Review or Sergei Kochkin, PhD, at.

Citation for this article:

Kochkin S. MarkeTrak VIII: 25-year trends in the hearing health market. Hearing Review. 2009;16(11):12-31.

References

- Hearing Industries Association. HIA Market Survey: A Summary of Findings and Business Implications for the US Hearing Aid Industry. Washington, DC: HIA; October 1984.

- Gallup Organization. A Survey Concerning Hearing Problems and Hearing Aids in the United States. Conducted for the Hearing Industries Association. Washington, DC: Hearing Industries Association; September 1980.

- US Department of Health and Human Services, Centers for Disease Control and Prevention. Prevalence and characteristics of persons with hearing trouble: United States, 1990-1991. Washington, DC: CDC. Series 10; No 188; March 1994.

- Agrawal Y, Platz EA, Niparko JK. Prevalence of hearing loss and differences by demographic characteristics among US adults. Arch Intern Med. 2008;168(14):1522-1530.

- Reuters News Service. US Hearing Loss Approaching Epidemic Proportions. Available at: www.hearingreview.com/insider/2009-04-09_04.asp. Accessed July 29, 2008.

- Niskar AS, Kieszak M, Holmes A, Esteban E, Rubin C, Brody D. Prevalence of hearing loss among children 6 to 19 years of age: The third National Health and Nutrition Examination Survey. JAMA. 1998;279(14):1071-1075.

- Kochkin S. MarkeTrak VII: Obstacles to adult non-user adoption of hearing aids. Hear Jour. 2007;60(4):27-43.

- Schein JD, Gentile A, Haase KW. Development and evaluation of an expanded hearing loss scale questionnaire. National Center for Health Statistics. Vital Health Stat 2. 1970;(37):1-42.

- Plomp R. Auditory handicap of hearing impairment and the limited benefit of hearing aids. J Acoust Soc Am. 1978;63:533-549.

- Koike J, Hurst MK, Wetmore SJ. Correlation between the American Academy of Otolaryngology-Head & Neck Surgery (AAO-HNS) five minute hearing test and standard audiological data. Otolaryngol-Head Neck Surg. 1989;111(5):625-632.

|

More on Trak

MarkeTrak VIII is the largest and most comprehensive database since its inception. Future publications in this series over the next few years will consist of the following:

- Customer satisfaction with hearing aids;

- Customer satisfaction with hearing health professionals and correlates of satisfaction due to differences in hearing aid fitting protocols and services;

- Customer satisfaction with open-fit hearing aids compared to traditional styles;

- Sources of noise that most impact satisfaction with hearing aids (essay analysis);

- Perceptions of benefit and changes in quality of life due to hearing aids;

- Impact of hearing loss and amplification on job performance, employability, promotions, and income;

- Safety as a function of demography and hearing loss;

- Prevalence of tinnitus in America;

- Perceptions of efficacy of tinnitus treatment techniques including hearing aids;

- Uses of assistive listening devices;

- Use of inexpensive listening devices (<$50) in lieu of hearing aid adoption;

- Factors that would influence hearing-impaired non-adopters to purchase and use hearing aids;

- Comparison of customer satisfaction in other professions and with products and services including hearing health professionals and hearing aids (non-adopter population only);

- Media habits of the hearing-impaired populations (owners and non-adopters); and

- Reasons for hearing aid returns (essay analysis).