By Karl Strom, editor-in-chief

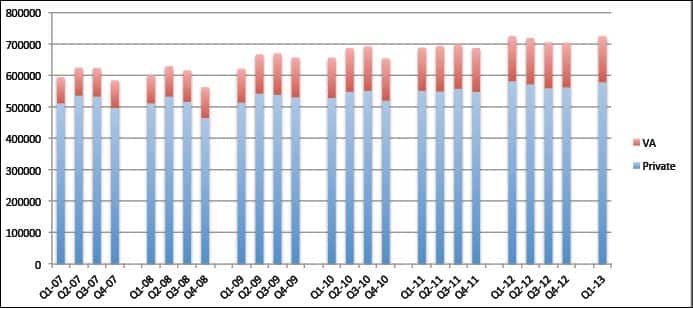

With a few notable wrinkles, US net unit sales of hearing aids in the first quarter of 2013 look a lot like those from the first quarter of 2012 (Figure 1). According to statistics compiled by the Hearing Industries Association (HIA), Washington, DC, a total of 724,853 hearing aid units were sold in Q1 2013, or 0.1% more than during the same period last year. Private sector (commercial non-VA) sales fell by a half-percentage point (0.5%) while units dispensed by the Department of Veterans Affairs rose slightly by 2.6% compared to Q1 2012.

Although it’s always nice to have something “big” to write about, the sales figures above are not particularly surprising, nor do would they evoke much more than a shrug from most dispensers and manufacturers. Last year’s first quarter sales were slightly better than average (a 5.3% gain compared to Q1 2011), and those gains were fueled primarily by private-sector sales. Thus, this year’s first quarter can probably be seen as “okay” or at least “business as usual.” Next month’s sales figures should provide a better bellwether for how 2013 will shape up—or not.

|

| Figure 1. US quarterly hearing aid net unit sales for the private-sector (blue) and the VA (red). Hearing aid sales in the first quarter of 2013 were essentially the same as the first quarter of last year. (click to enlarge) |

|

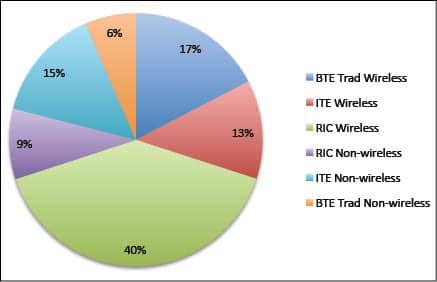

| Figure 2. Wireless versus non-wireless hearing aid market share divided into three product classes: traditional behind-the-ear (BTE Trad), in-the-ear (ITE), and receiver-in-the-canal or receiver-in-the-ear (RIC). Wireless hearing aids now constitute 70% of the total hearing instrument market, with wireless RIC/RITEs being the most-used device type. (click to enlarge) |

Wireless now 70% of market. Starting in the first quarter of 2013, HIA is tracking the use of wireless vs non-wireless hearing instruments. These new statistics show that wireless hearing aids now constitute 70.0% of the entire market. In the private-sector (non-VA), 65.1% of all units dispensed are wireless. Figure 2 shows the usage of wireless versus non-wireless hearing aids in the first quarter separated into three styles: in-the-ear (ITE), traditional behind-the-ear (BTE Trad), and receiver-in-the-canal or receiver-in-the-ear (RIC) device catagories. RIC/RITEs now constitute half (49%) of all hearing aid sales, and four-fifths (82%) of all RIC/RITEs use wireless technology. Traditional BTEs and ITEs essentially split the remaining half of the market into their respective quarters. The majority (73%) of traditional BTEs are wireless, while just less than half (46%) of ITEs are wireless.

I am surprised at how fast wireless hearing aids have come to dominate the market, and how pervasive they have become—even in the smaller ITEs. HIA statistics indicate that more than one-quarter (27.7%) of completely-in-the-canal (CIC) aids are wireless, half of all in-the-canal (ITC 50%) and full-shell ITEs (48%), and nearly three-quarters of half-shell ITEs (71%) employ wireless technology.