|

This month’s feature article by Brian Taylor, AuD, and Darrel Teter, PhD, about how to modify BTEs using vents, horns, and earmold tubing is another indication of the resurgence of the BTE. In fact, it is something of a “back to the future” article; Drs Taylor and Teter are rekindling the flames of interest on the important topic of earmold acoustics—an issue that some might regard as a “dead art” in light of the impressive menu of electroacoustic modifications that can be made with hearing aid programming software. Venting, horns, and earmold tubing have taken on a renewed importance in the era of mini-BTEs, and there’s good reason to look to the past for improving future fittings, as this article shows, as did the article on extending candidacy for thin-tube BTEs by Darrel Rose et al in the September 2008 edition of HR.

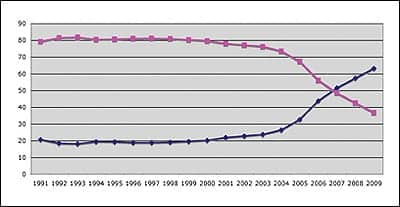

Speaking of “back to the future,” according to Hearing Industries Association (HIA) statistics, BTEs constituted nearly two-thirds (63.1%) of all the hearing aids fit during the first half of 2009 (Figure 1). Twelve years ago, in 1997, BTE market penetration was only 18.8%, and the percentages of BTEs rose fairly slowly until 2003, when ReSoundAir, Sebotek PAC, Vivatone, and several other BTE-related innovations started to appear on the market. From that point, BTE market share has climbed steeply, and it will continue for the near future. Although there is still plenty of room to grow, in all likelihood, BTE market share will not come close to matching the levels seen in Europe; for example, BTE market penetration is above 80% in France and Germany.

|

| FIGURE 1. Market penetration of BTEs (in blue) versus ITEs (in pink) from 1991 through the first half of 2009. After constituting about 20% of the market share for more than a decade, BTE popularity rose sharply after 2004. |

The HIA statistics also demonstrate how mini-BTEs, open fittings, and new BTE cosmetic options have played large roles in the popularity of BTEs. In the first half of 2009, 41.9% of all the BTEs sold (ie, 26.4% of the total market) used the smaller Size 10 and Size 312 batteries, and about 36.5% of all the BTEs (23.1% of total market) were RIC/RITE-type aids. As noted in Dr Taylor and Teter’s article this month, as well as in Rose et al’s article, there is potential to continue to extend the fitting candidacy of these BTE types through judicious use of earmolds and plumbing-related features; so, as with BTE styles in general, RICs and RITEs should continue to gain in popularity.

As reported in last month’s HR, hearing aid unit sales increased by 4.73% in the first half of 2009 compared to the same period last year, according to HIA statistics. However, when dispensing activity from the Department of Veterans Affairs (VA) is ignored, private sector hearing aid sales growth was only 1.7%. During the second quarter, overall unit sales increased by 6.8% (year-on-year), building on sales growth of 3.41% in the first quarter. Again, private sector sales growth was comparatively lower, increasing by 1.82% in the second quarter, after flat sales (0.43%) in the first quarter. Although these are not numbers that might prompt you to jump up and down with glee and boast that the recession is definitely over, it is worth noting that market conditions have improved significantly compared to the last three quarters of 2008.

Karl Strom

Editor-In-Chief