Staff Standpoint | May 2017 Hearing Review

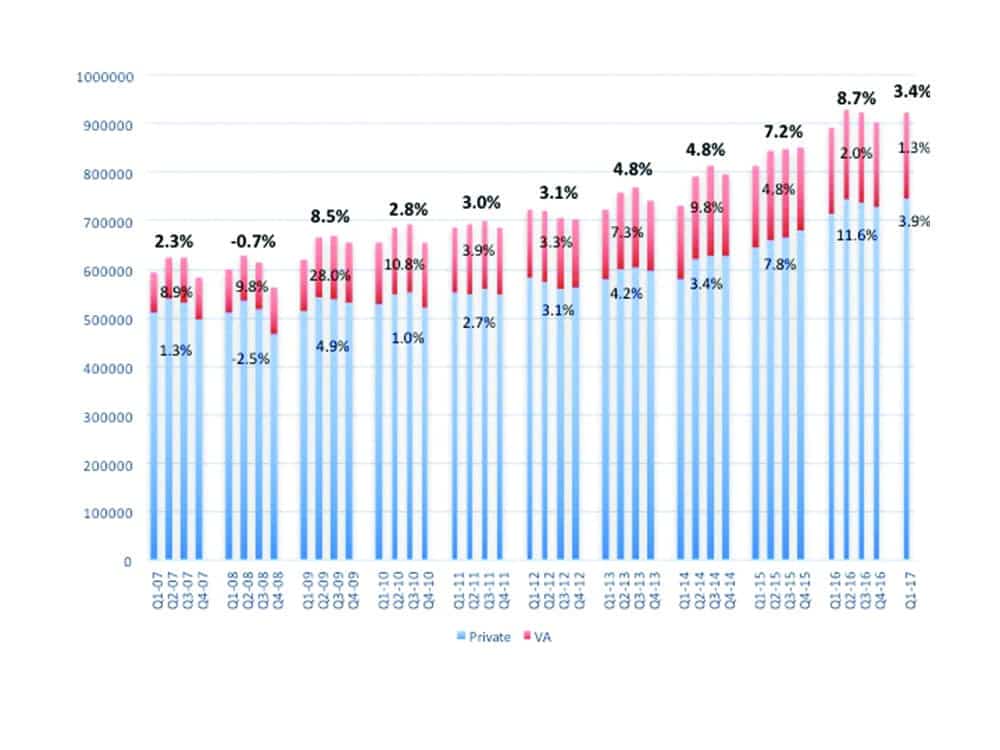

Figure 1. [Click on image to enlarge.] US net unit sales of hearing aids by quarter (2007-2017), with private/commercial unit sales shown in blue and VA dispensing in red. Overall percentage gains/losses for each year are shown in bold at the top. In the first quarter of 2017, total hearing aid unit sales increased by 3.4%, with a 3.9% gain for the private/commercial sector and a 1.3% gain for the VA.

This comes despite all the turmoil, in front of what appears will be a new FDA classification for over-the-counter (OTC) hearing aids (see article about the April 2017 FTC hearing). This edition of Hearing Review leads off with an abridged version of a study by Larry Humes and colleagues at Indiana University (the comprehensive study appears in the American Journal of Audiology) which has generated a lot of discussion in the field. Although the study’s methodology may not be exactly representative of what most would view as a “typical OTC model” (eg, pre-screened subjects using high-quality hearing aids), it sheds light on many interesting facets of the OTC debate. The one that is generating a lot of controversy is that the Audiology Best-practices (AB) group and the Consumer Decides (CD/OTC) group had no significant differences in terms of speech recognition or subjective benefit. But is this really surprising? After all, dispensing professionals know that audibility matters. And, as the study also abundantly points out, so does the addition of professional care; the AB group which received services associated with audiology best practices were found to have higher satisfaction scores, and 81% of the AB group purchased their hearing aids compared to only 55% of the CD/OTC group (also see p 27 for a discussion of the study relative to teleaudiology by Stender, Groth & Fabry).

With the FDA, FTC, and other stakeholders in the OTC debate moving quickly (see p 8), keep looking to HearingReview.com for more information on these important issues.

Citation for this article: Strom KE. Growing market, despite turmoil. Hearing Review. 2017;24(5):8.