Practice Management | September 2021 Hearing Review

Part 1: An introduction to managed care and its many parts and permutations

By Carrie Meyer, AuD

While provider participation in managed care remains optional, managed care is now an integral part of US healthcare. Hearing care as a supplemental benefit will continue to grow in private and public health plans. As healthcare providers, it is critical that audiologists and hearing aid specialists understand the dynamics of managed care and become well informed to make the best decisions for their practices and their patients in this rapidly changing healthcare environment. Part 1 of this 3-part series is a primer on health insurance and managed care.

Managed care is an important and challenging topic for hearing healthcare professionals (HCPs). As the health plan market continues to expand—especially Medicare Advantage plans aimed at the ever-growing senior market—audiologists and hearing aid specialists find themselves in a constantly changing environment. With fewer patients willing to pay full price out of pocket for hearing aids, practices are struggling to balance expectations for revenue against the actuality of smaller reimbursements. Audiology social media platforms are full of conversations, anecdotes, and the occasional tirade about managed care. Like much of the digital world, there are excellent sources of well -esearched information online as well as a significant amount of misinformation about managed care and health plans with hearing benefits.

This series of articles will cover insurance-related topics to help HCPs make well-informed decisions about whether to participate in a managed care network. This first article is a primer on health insurance and managed care. The next article will investigate the recent growth of managed care and the expansion of supplemental benefits, such as dental, vision, and hearing care. We will compare common perceptions and realities of managed care among hearing healthcare providers. The final article in this series will explore ways to build a successful and sustainable practice while participating with managed care, and highlight the benefits of participation (yes, there are benefits).

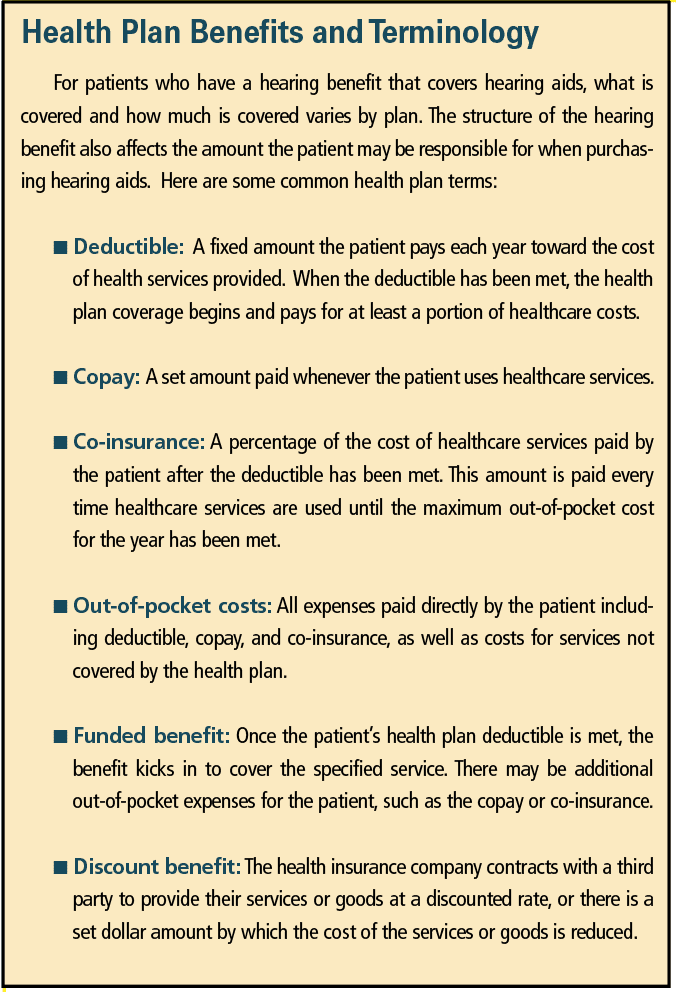

US Health Insurance Overview

This first article is designed to demystify the complex world of managed care and provide basic information that serves as a building block for the subsequent articles in this series.

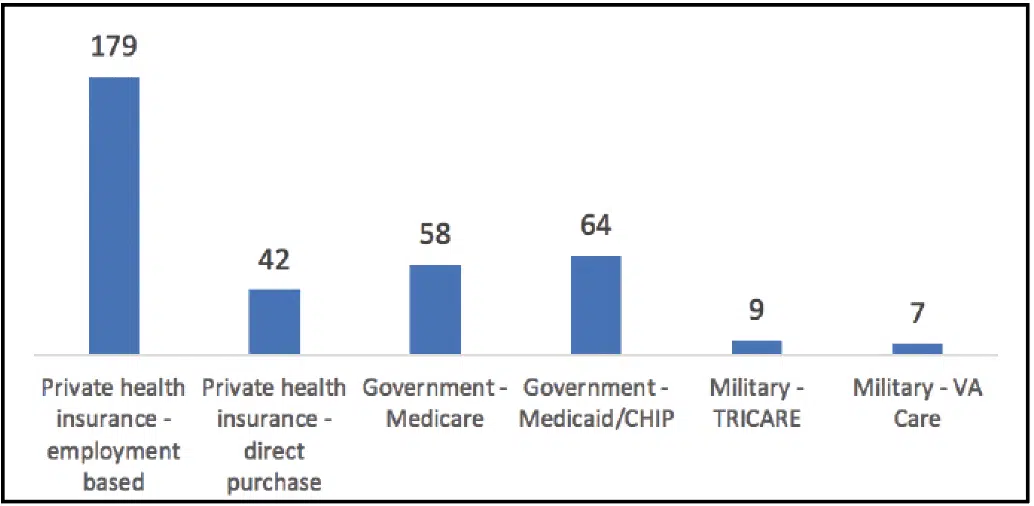

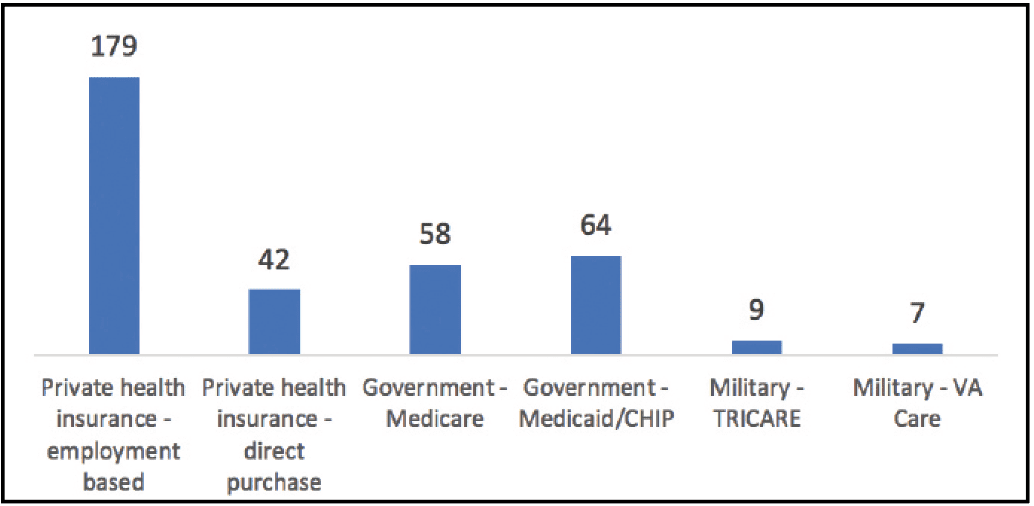

In the United States, there are two types of health plans: private and government. Private health plans (also referred to as “commercial”) are often provided by an employer and administered by a non-governmental entity or private health insurance company. As shown in Figure 1, 55% of Americans with health insurance have an employer-sponsored plan. In addition to employer-sponsored health plans, individual plans can be purchased directly from a health insurance company or through the Health Insurance Exchange (Marketplace). About 1 in 8 Americans (13%) with health insurance have an individual plan.

Figure 1. Enrollment in the United States by type of insurance coverage, 2019. Note that individuals may have more than one type of coverage at a time (for example, Medicare and Medicaid). Therefore, estimates by types of coverage are not mutually exclusive.

Government or public health plans are provided by the government for low-income individuals or families, people age 65+, and others who qualify for special subsidies. The primary public health programs are Medicare, Medicaid, TRICARE, VA, and Children’s Health Insurance Program (CHIP). About 35% of Americans with health insurance have a public plan.

Managed Care

Almost all US health plans are managed care plans. Managed care plans are designed to manage healthcare quality and costs by shifting excessive utilization of resources toward less costly and more effective treatments. The primary way managed care plans work is by first establishing provider networks. The health insurance company contracts with providers and medical facilities in these networks to deliver care for patients at a reduced cost.2

Along with standard medical services, an increasing number of managed care plans offer supplemental benefits including vision, dental, and hearing. For health insurance companies, offering supplemental benefits gives patients access to affordable care and services that improve health and reduce overall medical costs. As an example, a recent study published in JAMA showed that older adults with untreated hearing loss experience 46% higher healthcare costs.3

With cost cited as one of the primary barriers to care for people with hearing loss, having a plan with a hearing benefit is the single biggest motivator to purchase hearing aids.4 With a hearing benefit, more people with untreated hearing loss should be able to afford hearing aids.

Types of Managed Care Plans

In general, there are five types of managed care plans: HMOs and PPOs, Medicare (Parts A-D), Medicaid, TRICARE for veterans and military members, and TPAs. The remainder of this article will look at each, and also examines the terminology used in managed care.

HMOs and PPOs

1) Health Maintenance Organizations (HMOs): HMOs require patients to choose one primary care physician who serves as the central provider and coordinates the patients’ care with other specialists.5

2) Preferred Provider Organizations (PPOs): PPOs contract with providers and medical facilities to create a network. Patient out-of-pocket costs and deductibles are less if in-network providers are used, but out-of-network providers are covered, albeit at a higher out-of-pocket cost for the patient.5

For PPOs there are two types of providers:

a) In-network Provider: A healthcare provider who is part of a health insurance company’s network of providers. This provider has signed a contract with the health insurance company and agrees to accept their negotiated fees. Patients enrolled in the health insurance company’s plans are referred to in-network providers. For participating providers, this is a no-cost source of patient referrals.5

b) Out-of-Network Provider: A health- care provider who is not part of a health insurance company’s network of providers. This provider has not agreed to accept the health insurance company’s negotiated fees. Patients enrolled in the health insurance company’s plans may still receive services from an out-of-network provider, but the patient will be responsible for all or a greater portion of the cost.5

Medicare and Its Parts (A-D)

Since its inception in 1965 as part of the Social Security Act Amendments signed by President Lyndon Johnson, Medicare has provided coverage for hospital and physician services to people 65 and older. Medicare was created as a basic health plan and did not include hearing loss or hearing aids when it went into effect. Today, Medicare has four parts6:

- Medicare Part A provides inpatient/hospital coverage. This includes inpatient hospital care, skilled nursing facility care, home healthcare, and hospice care.

- Medicare Part B provides outpatient medical coverage. This includes services from licensed healthcare professionals, durable medical equipment, home health services, ambulance services, preventative services, therapy services (eg, physical, occupational, and speech therapy), and mental health services. Medicare Part B also covers x-rays and lab tests, chiropractic care, and some prescription drugs that must be administered by a physician, such as chemotherapy or dialysis drugs. Currently, Medicare Part B does not cover hearing aids.

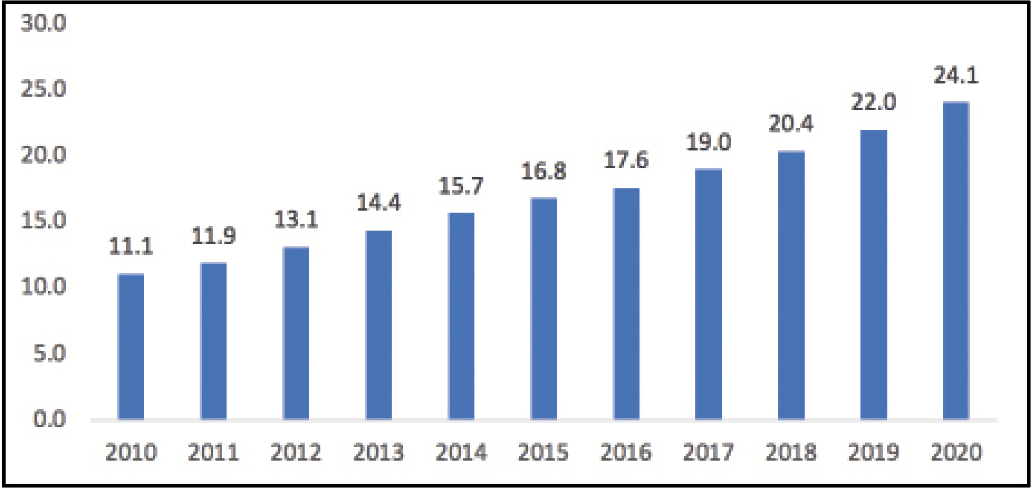

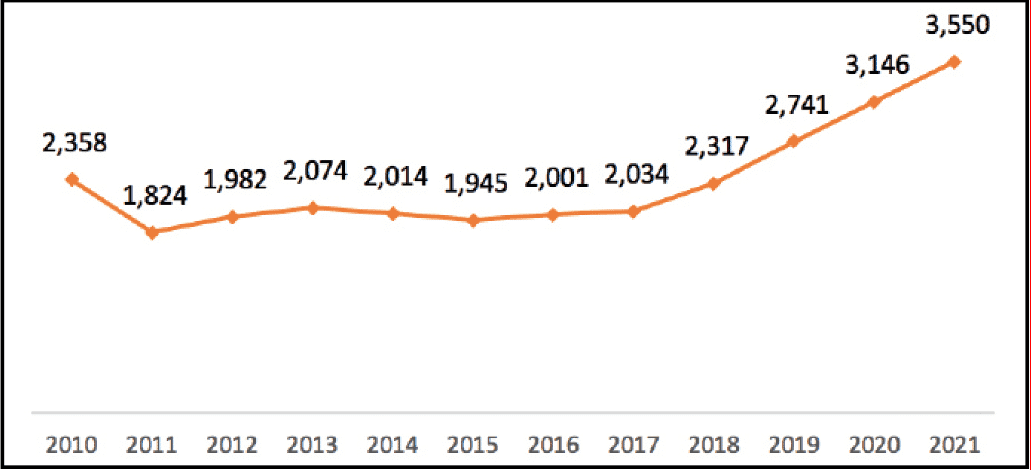

- Medicare Part C or Medicare Advantage plans are offered by private health insurance companies that contract with the federal government and are paid a fixed amount per person to administer Medicare benefits. Medicare Advantage plans must provide the same level of coverage as standard Medicare. These plans, which continue to grow in popularity (Figures 2 and 3), control costs by operating as either a PPO or an HMO, so patients must use a network provider for care. One of the most attractive features of Medicare Advantage plans is the inclusion of ancillary benefits for care services not covered by traditional Medicare, like hearing aids.

Figure 2. Number of Medicare Advantage enrollees (in millions of lives), 2010-2020.7

Figure 3. Number of Medicare Advantage plans, 2010-2021.8

- Medicare Supplement Plans (also called Medigap) are plans available from private health insurance companies in most states. Medigap plans are designed as a supplement, to be used in addition to traditional Medicare, and cover out-of-pocket costs, including copayments, co-insurance, and deductibles. Medicare Supplement plans generally do not provide coverage for ancillary services such as vision, dental, and hearing. If the supplement plan does include these additional benefits, it is usually in the form of a discount plan.

- Medicare Part D covers most outpatient prescription medications. Part D, like Part C, is offered through private health insurance companies either as a standalone plan for patients with original Medicare (Part A and Part B), or prescription benefits included in Medicare Advantage plans.

Medicaid/Medical Assistance

Medicaid is health coverage jointly financed by the state and federal government. Medicaid provides health insurance for eligible low-income adults and children, pregnant women, elderly adults, and people with disabilities. Eligibility is based on income. Most Medicaid programs are administered by health insurance companies that contract with the state to provide services.

Medicaid programs provide hearing aids for children in most states and for adults in many states, depending on the individual state plan. According to the American Speech-Language-Hearing Association (ASHA), 23 states mandate that health insurance companies must provide at least partial coverage for hearing aids for children.9 Five states (Arkansas, Connecticut, Illinois, New Hampshire, and Rhode Island) also extend those mandates to adults.

Children’s Health Insurance Program (CHIP) provides low-cost health coverage to children in families that earn too much money to qualify for Medicaid. In some states, CHIP covers pregnant women. Each state offers CHIP coverage and works closely with its state Medicaid program.

Military Members and Veterans

Veterans who are eligible to enroll, receive the Department of Veterans Affairs’ (VA) comprehensive Health Benefits Package which includes preventive, primary, and specialty care; diagnostic, inpatient, and outpatient care services. Veterans may be eligible for additional benefits, including hearing aids, depending on their individual situation and if their hearing loss is determined to be service-related.

Depending upon their status, active-duty military members, retired service personnel, members of the Guard/Reserves, family members, and certain veterans receive no-cost or government-subsidized medical and dental care through the federal program TRICARE. TRICARE may cover hearing aids and hearing aid services for active-duty service members and family if specific hearing loss criteria are met.10

Third-party Administration

A Third-party Administrator (TPA) is a company that provides administrative services on behalf of a health insurance company. Examples of administrative services include enrollment and eligibility management, claims processing, benefit design and administration, customer service, regulatory compliance, and utilization management. The TPA may also offer network management services which include recruitment, credentialing, and education about the hearing benefit so providers can deliver care to patients with coverage through the health insurance company.

Summary

Managed care is intended to reduce the cost of healthcare and health insurance while improving the quality of care patients receive. It has become the primary system of delivering and receiving health care in the United States since its implementation in the early 1980s. Today, its impact continues to expand as policy makers, academic researchers, healthcare professionals, and patients work to bend the healthcare cost curve towards greater efficiency and value.11

While provider participation in managed care remains optional, managed care is now an integral part of healthcare in the United States. Hearing care as a supplemental benefit will continue to grow in private and public health plans. As healthcare providers, it is critical that audiologists and hearing aid specialists understand the dynamics of managed care and are well informed to make the best decisions for their practices and their patients in this rapidly changing healthcare environment.

CORRESPONDENCE can be addressed to HR or Dr Meyer at: [email protected].

Citation for this article: Meyer C. How to manage in managed care. Hearing Review. 2021;28(9):24-27.

References

- United States Census Bureau. Health insurance coverage status and type of coverage by state-All persons: 2008 to 2019 [Table HIC-4_ACS]. https://www.census.gov/data/tables/time-series/demo/health-insurance/historical-series/hic.html. Published September 2020.

- Tobin C. What is managed health care? AADE News. 1997;23(1).

- Reed NS, Altan A, Deal JA, et al. Trends in health care costs and utilization associated with untreated hearing loss over 10 Years. JAMA Otolaryngol Head Neck Surg. 2019;145(1):27-34.

- Mueller G, Carr K. 20Q: Consumer insights on hearing aids, PSAPs, OTC devices, and more from MarkeTrak 10. AudiologyOnline. https://www.audiologyonline.com/articles/20q-understanding-today-s-consumers-26648. Published 2020.

- Health Maintenance Organization Act. H.R.7974 (1973).

- Medicare website. What’s Medicare? https://www. medicare.gov/what-medicare-covers/your-medicare-coverage-choices/whats-medicare.

- Freed M, Damico A, Neuman T. A dozen facts about Medicare Advantage in 2020. Kaiser Family Foundation (KFF) website. https://www.kff.org/medicare/issue-brief/a-dozen-facts-about-medicare-advantage-in-2020/. Published January 13, 2021.

- Biniek JF, Freed M, Damico A, Neuman T. Medicare Advantage 2021 spotlight: First look. Kaiser Family Foundation (KFF) website. https://www.kff.org/medicare/ issue-brief/medicare-advantage-2021-spotlight-first-look. Published October 29, 2020.

- American Speech-Language-Hearing Association (ASHA) website. State insurance mandates for hearing aids. https://www.asha.org/advocacy/state/issues/ha_reimbursement/.

- TRICARE website. Covered services: Hearing aids. https://tricare.mil/ CoveredServices/IsItCovered/HearingAids. Published June 18, 2020.

- Kauffman L. Feature report: Hearing and value-based healthcare. https://hearingreview.com/wp-content/uploads/2018/03/ValueBasedHearingCare_FeatureReport_0318HR.pdf. Published 2018.