Figure 1. [Click on graphics to expand.] US hearing aid unit sales, 2007-2017. Percentages represent year-on-year increases/decreases in net units for the entire market (top bold), the VA (red), and the private/commercial sector (blue). Source: HIA.

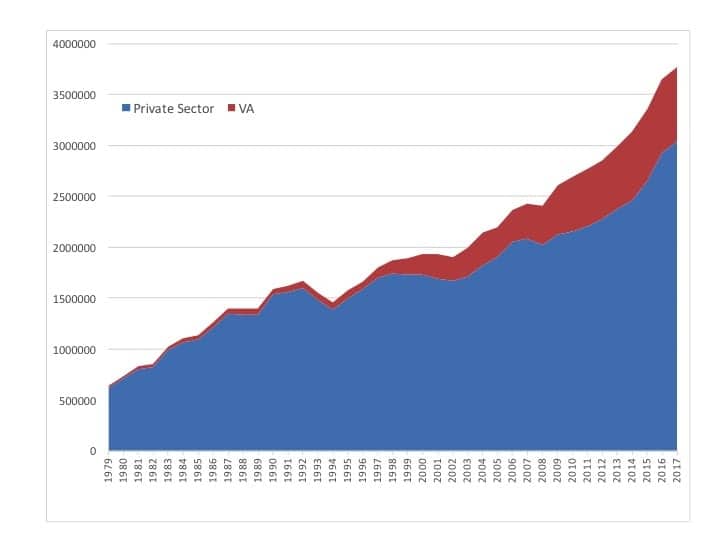

Figure 2. US net hearing aid sales, 1979-2017. The VA made up 19.3% of the total US market in 2017.

Sales growth was particularly strong during the fourth quarter of 2017, with a 6.0% increase over the same period last year—powered by a 7.3% increase in unit sales for the private sector. The VA saw its units increase by 0.9% in Q4.

Because private-sector sales also encompass mass merchandisers like Costco—and hearing aid sales statistics are unavailable for these retailers—it has become increasingly difficult to guess how the “average” private-practice dispensing office fares during the year. If Costco continued at the 8% growth rate Hearing Review estimated for 2016, that would mean mass retailers probably account for about 12% or more of all hearing aids dispensed, and the average dispensing practice saw actual unit gains of around 3.4% in 2017. Again, it should be emphasized that these estimates are “guesses” by the editor. Additionally, it should also noted that average selling prices (ASPs) of hearing aids have been declining on average by 1-2% annually (or more), so net revenues for many businesses may have been relatively flat.

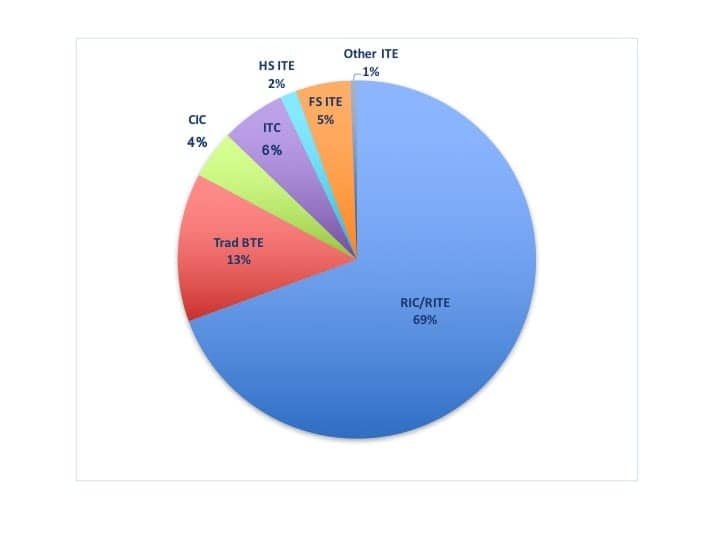

Styles of hearing aids dispensed for the entire US market (VA + private sector) in 2017. RIC/RITE hearing aids made up over two-thirds of the market.

According to the HIA statistics, a total of 82.8% of all hearing aids dispensed in 2017 were behind-the-ear (BTE) style devices, and over two-thirds (69.4%) of these were of the receiver-in-the-canal (RIC) or receiver-in-the-ear (RITE) style (subclasses of BTEs). Traditional BTEs constituted 13.4% of all hearing aids sold.

In-the-ear (ITE) hearing aids made up less than one-fifth (17.2%) of the entire market in 2017. In-the-canal (ITC) type aids constituted 5.8% of all the units sold, full-shell ITEs (4.9%) and half-shell ITEs (1.5%) made up a similar proportion, and CICs accounted for 4.4% of all hearing aids sold, according to HIA. —KES