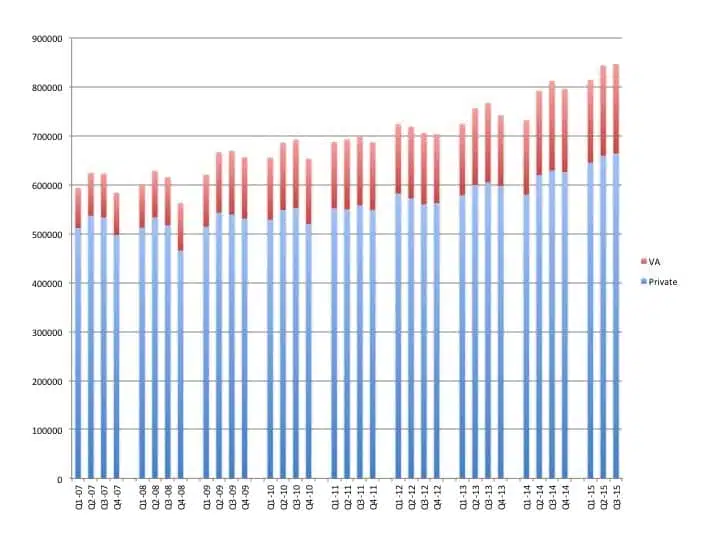

US hearing aid sales increased by 4.2% in the third quarter of 2015, aided by a 5.6% increase in private-sector dispensing, according to statistics generated by the Hearing Industries Association (HIA), Washington, DC. However, dispensing activity at the Department of Veteran Affairs (VA) was flat (-0.4%), dipping into negative territory for the first time in almost a decade (Q1 2006).

For the overall hearing aid market in 2015, unit sales are up 7.2%. Unit growth in the private/commercial sector has maintained a steady clip throughout 2015, totaling a 7.7% growth rate through the first three quarters. So far this year, private-sector sales have experienced excellent, albeit diminishing, quarterly increases of 11.32%, 6.4%, and 5.6% compared to the Q1-Q3 2014. However, it should be noted that Big Box retail is also included in this number, so the percentages do not necessarily reflect what is occurring within the traditional professional channel.

BTEs made up nearly four-fifths (79.0%) of all hearing aid unit sales through the first three quarters of 2015 (80.0% private sector; 75.1% VA). Of those BTEs, 80.7% featured external receivers and 84.2% featured wireless technology.

No real change in return for credit (RFC) rates have occurred this year; about 1 in 5 of all hearing aids (19.8%) were returned in Q3 2015. ITE wireless hearing aids were the most likely to be returned (an RFC of 24.9%), followed by ITE non-wireless (21.1%), BTE wireless (19.2%), and BTE non-wireless (16.3%).

Thanks for your comments, Alex and Gabriella. The HIA statistics are broken into two categories: VA and commercial/private-sector sales. As such, they don’t offer any real glimpses into big box vs independents vs 3rd parties, etc. I agree that it would be nice if they would, but in our highly competitive market, I think HIA reporting members would be reluctant to share or make public that granular type of sales data. Likewise, HIA does not monitor or publish any trend data on ASPs of hearing aids. The last dispenser pricing survey I’ve seen on this was published in The Hearing Review in April 2014. Most market analysts say that ASPs have been falling for the past several years by 1-2%; however, it’s unclear whether that’s due to greater VA market penetration (and, worldwide, other reimbursement systems like NHS in the UK) or factors like Big Box retail, etc.

The HIA statistics, however, do offer some insights into state-by-state unit sales for the US private/commercial sector. To be honest, I don’t routinely report on this data because it’s often all over the board and requires quite a bit of time and space to both publish and for readers to digest. We last published a regional and state-by-state summary of hearing aid sales in the May 2013 Hearing Review, and there is a 10-year trends summary of state-by-state sales in the “What Works” Toolkit offered at the CareCredit booth at AAA, IHS, and ADA.

Hope this helps. Thanks again for your readership.

It would be beneficial to see a few more pieces of data here. What numbers are related to private practice, and are they up, and if so, how much over last quarter and last year this time? What numbers are related to big box, etc? What I would find valuable, as may others, is what areas of the country are up, flat, or down? Is California up? Is New Jersey flat? Etc.

What I would like to know, and what is not mentioned in this article is what do they think may contribute to the increase in sales.

I personally think this is due to more beneftis being offered. I also would like to see a report in the national average in the cost of the devices sold and what percentage is due to 3rd party (Epic, Hear PO, TruHearing, etc.) and how this affects the private practice bottome line.

Gabrielle