In 2003, hearing instrument sales increased substantially for the first time in nearly 5 years. Unit sales came within a breath of reaching the 2-million mark. Hearing aid sales in the third and fourth quarters experienced double-digit growth, and it was the first time in industry history that unit sales exceeded a half-million units in consecutive quarters. When VA sales are ignored, private practice unit sales rose by 2.6%. This article takes a long-term look at the market, analyzes the influence of digital aids, and speculates on what might be a brighter future for the hearing industry.

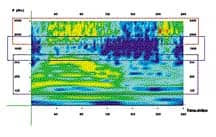

During the second half of 2003, the US hearing industry pulled itself out of a relatively poor 5-year sales period to post a yearly net unit volume gain of 4.94%, according to statistics generated by the Hearing Industries Association (Figure 1). A total of 1,997,139 hearing aids were dispensed in 2003—which means that the industry came within a rounding function of reaching the 2-million unit mark for the first time ever. When including exports, hearing aid unit volume totalled 2.08 million units, a 5.07% increase over 2002.

Figure 1. US hearing instrument quarterly unit sales (top) and quarterly percentage gains/losses (bottom) relative to the previous year, 1990-2003. Until the second half of 2003, unit sales have been in a holding patter for nearly 5 years, with a mean annual growth rate of only 0.35% from 1999-2002. Source: Hearing Industries Association (HIA).

Even more impressive, during the second half of the year, the industry saw its most robust sales increases since 1995 (Figure 1). Third Quarter hearing aid sales exceeded previous records for unit volume (501,900 units) and percentage increase over the previous quarter (12.1% higher than in Q3 2002). The Fourth Quarter (9.8% higher than Q4 2002) continued on this strong trend, making it the first time in industry history in which unit sales exceeded a half-million units in consecutive quarters.

Despite these cheery statistics, when government dispensing activities (ie, Veterans Administration) are ignored, hearing aid sales for private practices increased by only 2.63%. Assuming that the average hearing care office/practice dispenses 20 hearing aids per month, this roughly translates into about 6 more hearing aids sold per office in 2003 compared to 2002—or a gross revenue increase of about $10,800.

VA sales of hearing aids in 2003 increased by a substantial 21.2% after almost no dispensing growth for the agency during 2001-2002. In total, this extra unit volume from the VA accounted for 53.4% of the entire industry’s market growth. The agency is now responsible for more than 1-in-7 (14.4%) of all the hearing aids dispensed in the US.

DSP Market Comes of Age

Figure 1 shows the quarterly US net unit sales of hearing instruments during the last 14 years. During this timespan, the hearing instrument market has grown by 406,000 units (25.5%) to its current annual sales of just under 2 million units. Clearly shown in Figure 1 are two extended periods that were marked by flat or declining sales: 1) a 2-year period from Q1 1993 ending with Q4 1994, and 2) a nearly 5-year period from Q4 1998 ending Q3 2003. The first period of sales decline has been widely attributed to negative publicity generated by FDA involvement in the hearing industry relative to hearing aid advertising claims; the agency’s 510k advertising requirements that led to confusion within the industry, reduced advertising, and delayed product introductions; and a hailstorm of bad press, public hearings, and professional infighting.

The latter period of stagnant market growth—from which the industry is now hopefully emerging— may be a bit more complex to explain. Prior to the second half of 2003, the hearing industry had experienced unit volume decreases in 7 of its last 10 business quarters. In fact, from 1999 to 2002, US hearing aid sales grew by only 1.4% (26,000 units), with a mean annual growth rate of 0.35%. Several explanations have been proposed as reasons for these lagging sales, including the economy, anomalies in the population statistics of those over age 55, and a reduction in advertising by the retail chains (eg, Beltone, Miracle Ear).

Figure 2. US net unit hearing instrument sales by technology type: digital (DSP), programmable analog, and non-programmable analog instruments. In 2003, digital hearing aid sales grew to make up 66% of the market, compared to only 14% for programmable hearing instruments, and 20% for analog non-programmable hearing instruments.

However, one of the more compelling explanations for the reduction in units dispensed is the introduction and widespread popularity of digital signal processing (DSP) hearing aids. DSP aids were first introduced in 1996 but did not enjoy substantial use until 1998 (Figure 2). Interestingly, the largest initial impact of DSP was to draw attention to and increase the market share of analog programmable instruments.

Programmable instruments, from their introduction in the late-80s and throughout the early-90s, occupied a small niche (ie, less than 8% prior to 1995) in the market. However, by the late 90s, it was apparent that programmable instruments—whether analog or digital—would be the future of dispensing. It was only a matter of when the technology would be embraced by dispensing professionals.

When DSP aids were introduced in 1996, they completely changed the market. Coming in at around $2100, digital aids in 1996 were about $500 more expensive than programmable aids, and represented a clear premium product offering (along with the pizazz associated with DSP). It also gave many dispensing professionals more confidence when presenting their technologies and corresponding pricing to clients: with the advent of a $2100 DSP hearing aid, a $1600 programmable aid no longer seemed quite so expensive. A clear “good/better/best” (analog/programmable/DSP) product offering emerged. At the same time, many dispensing professionals came to embrace programmable compression technology, particularly WDRC, and recognized that the analog programmable aids of the late-90s provided similar advantages and features of the first-generation digital products. The result was that the analog programmable instrument market share grew relatively quickly over a 5-year period, from 12% in 1996 to 32% at the technology’s peak in 2001.

The influence of DSP instruments on hearing care practices was unmistakable. Digital aids went from a few percentage points in market share during 1996 and 1997 to a commanding share of the market (45%) by 2001 (Figure 2). As with any new technology, there appears to have been a period of adjustment in which dispensing professionals labored to learn how to fit the aids. For example, return rates soared into the high-20% region relative for some models of DSP aids. With the higher prices of DSP aids also came greater profit margins, and some people in the industry have maintained that these factors led to fewer units being dispensed.

About two-thirds (65.8%) of all hearing aids dispensed in 2003 were DSP instruments, up from 45% in 2002 (Figure 2). In fact, Fourth Quarter sales of DSP aids constituted 73.1% of the market. In other words, it is likely that more than 3-in-4 hearing aids (more likely, about 4-in-5) dispensed during 2004 will be digital. When comparing 2003 and 2002 unit volumes, digital hearing aid sales increased by 55%, while the use of programmable aids fell by 18% and the use of analog non-programmable aids fell by 30%.

Implications for industry? Until only a few years ago, most digital product lines were concentrated in the premium product segment of the hearing aid market, offering the highest technology and most sophisticated features at premium prices. Today, the digital hearing aid market has essentially reached maturity. Many hearing aid manufacturers now have product lines that span the complete range of features and price points—from premium high-end DSP lines touting all of the latest gadgetry to economical “value oriented” DSP devices and even to specific product niches (eg, power aids, etc) within product categories (Figure 3). The movement of DSP into the mid-level and value-oriented markets has brought these products into competition with most programmable and many analog non-programmable product lines, resulting in a severe squeezing of analog market share.

Thus, the prognostications of some industry experts in the mid-90s who predicted that programmable analog aids would be replaced by DSP instruments may yet prove to be true. Although analog programmable aids will remain a component of the market for years to come (they now constitute 14.0% of all aids dispensed), they may one day be viewed as a transitional technology that allowed for the first widespread use of WDRC and other advances. Many engineers state that, among the advantages that digital chips have to offer, is the fact that they can be produced relatively inexpensively when done so in large quantities; therefore, it’s conceivable that the entire market will be digital at some point.

Recent introductions of DSP product lines into the middle and value-oriented sectors have also place pressure on smaller hearing aid manufacturers. Between 1998-2002, a number of hearing aid manufacturers did remarkably well by astutely finding market niches in which their traditional analog and programmable analog instruments were well-suited (usually outside of the premium DSP product segment). With the expansion of digital product lines, these smaller manufacturer’s products are now going head-to-head with new digital offerings. In some cases, newly launched digital products appear to have been specifically targeted to compete against one or two analog programmable product lines. It should be noted that some smaller manufacturers have inherent advantages in catering to the service aspects and the unique needs of certain dispensing offices—in other words, it’s by no means all about technology and the depth of a company’s product offerings. However, it seems reasonable to conclude that those companies with a wide product selection running throughout the gamut of premium, middle, and value-oriented DSP products—as well as those who continue to maintain or find new product niches—are best positioned for the future.

Implications for private dispensing. As DSP product lines continue to move into the value-oriented segments of the market and more of these aids are sold, the average sales price (ASP) of hearing aids has flattened substantially. HR estimates that the average price of a hearing aid in 2003 was close to $1800, an increase of only $70 (4.0%) over the average price in 2002 ($1730). The HR 2003 Dispenser Survey indicated that prices for digital aids in 2002 actually fell by $231-$320 (about 10%-12%) in the ITE, ITC and CIC types, while they remained about the same for digital BTEs (possibly due to more directional microphones being employed in these models).

While lower prices may sound like trouble for the industry and dispensing offices, the much larger numbers of patients choosing digital aids or switching to digital in 2002-2003 buffered the impact of this trend. Although the retail price of hearing aids went down, once the large volume of more expensive digital aids are considered, the actual dollar values on a retail level remained fairly robust.

When applying the dollar values of each instrument type and technology shown in the 2003 HR Dispenser Survey to HIA sales statistics (including estimates of VA hearing aid dispensing activity), the US retail market value of hearing aids during 2003 was about $3.18 billion. This represents a 7.39% increase in retail dollar growth compared to 2002 when the estimated retail market value was $2.96 billion. (Editor’s note: Estimates by HR of average retail gross revenues are derived by applying the average price of each instrument type as reported in the annual HR Dispenser Survey and extrapolating them to HIA sales statistics for those instruments. It is important to note that considerable variations may exist in these estimations due to the predominant practice of “bundling” testing and service fees within hearing instrument prices (ie, in the annual HR Dispenser Survey, prices for both instruments and services are usually reported as the “hearing instrument price”). Additionally, third-party discounts, leasing programs, and free-hearing aids may significantly affect retail values. Thus, the retail dollar values are offered here only as a useful gauge for the actual dollar volume of the US market.)

State-by-state dispensing activity: Increases in dispensing activity were fairly well distributed across the US in 2003. Forty-seven of the 50 states in the union enjoyed sales increases over 2002 figures, with only Idaho, Oregon, and Rhode Island experiencing nominal (<1%) sales decreases. In terms of regional dispensing performance, five states in the Central Plains (MN, WI, MI, ND, SD, and MO), four in the Southeast (VA, NC, GA, and TN), three in the Northwest (WA, MT, and UT), and three in the South (AL, LA, OK) experienced net unit volume sales increases of 10% or more compared with 2002 sales.

Changes in hearing aid styles. Changes in hearing aid styles and technologies were also reflective of the growing dominance of DSP instruments. Preference for the overall styles of hearing aids changed little. BTE use continued to increase by about one percentage point in 2003 to constitute 23.7% of the market, while ITC use declined by about a like amount to make up 21.2% of the market. However, when looking at the DSP growth, it is very evident that digital instruments are rapidly cannibalizing sales from the analog and programmable categories.

DSP: The Double-Edged Sword

The importance that DSP instruments have assumed for the “typical” dispensing office is apparent in Figure 4. Not only have unit volumes of digital aids increased, but the gross revenues of the typical hearing aid practice are now extremely dependent on the sale of DSP aids. In the typical dispensing office, unit volumes of DSP aids during 1999-2003 increased from 13% to 66%, while gross revenues derived from the dispensing of DSP aids increased from one-fifth (22%) of dispensing revenues in 1999 to over three-quarters (78%) of revenues in 2003. In other words, when ignoring office sales from diagnostic services, batteries, ALDs, etc (which typically make up less than 10% of revenues for most practices/businesses), digital aids accounted for almost 4-in-5 of the dollars earned.

In contrast, gross revenues generated from analog and programmable aids have fallen precipitously. In 1999, non-programmable analog aids made up 61% of the units dispensed in an average hearing care office and accounted for 43% of gross revenues. By 2003, these hearing aids accounted for only 20% of the hearing aids dispensed and 11% of the gross revenues. Similarly, in 1999, analog programmable instruments constituted 26% of the net units dispensed and 35% of gross revenues; by 2003, these numbers had fallen to 14% and 11% respectively.

Obviously, the influence of digital technology on the hearing industry has been dramatic. In some ways, DSP technology has been a double-edged sword to the industry and dispensing professionals: in the long-term increasing the potential for higher levels of customer satisfaction and greater market penetration, while in the short term increasing the average cost of hearing aids, decreasing unit volumes, and cannibalizing analog market share.

Reasons for Optimism

Hearing aid technology has never been more sophisticated and effective; hearing care services have never been so advanced and reputable; and hearing instrument prices are essentially holding steady or declining. At the same time, it appears there may be a backlog of patients from the last 5 years, the economy looks like it’s on the mend, fears about war are starting to abate, and consumer confidence is on the rise (along with a fickle stock market). Maybe things aren’t so bad after all.

Additionally, hearing aid unit volume increased by almost 5% in 2003—almost all of the gains occurring in the second half of the year when double-digit growth occurred. As the number of amplification options for consumers increase and the price of advanced technology aids comes down, it’s reasonable to hope that there are considerable incentives for consumers to re-explore the purchase of hearing aids.

Pent-up demand and first-time users. By far, the number-one determinant for the 2003 hearing instrument market will be if the hearing care industry and dispensing professionals can attract the attention of first-time hearing aid purchasers. HR statistics point out that only 41% of consumers who purchased a hearing aid in 2002 were first-time users—an all-time low. First-time users have fallen steadily since the early-1980s when they constituted over three-quarters of hearing aid purchases.

Physicians’ awareness, positive press, and the Hearing Aid Assistance Tax Credit. The hearing industry has been blessed with amazing press in the last 3 years: the NCOA study on the influence that hearing aids have on an individual’s quality of life, the VA study on hearing aid efficacy published in JAMA, and the 2003 JAMA articles by Yeuh et al. on why physicians should screen for hearing loss were unparalleled for the field. By all indications, the medical community—with considerable help from the Better Hearing Institute’s Physicians’ Referral Program and its dispenser participants—is beginning to appreciate the vital need for appropriate hearing care and amplification.

As monumental as the above are for encouraging consumers to address their hearing health, the Hearing Aid Assistance Tax Credit (HR 3103) has the potential to completely transform the hearing care field. Although it is unlikely to be passed immediately, even a public discussion of the bill—which calls for a $500-per-hearing aid tax credit (usable once every 5 years for those over age-55 and for children)—would thrust hearing health care into an extremely positive light (as long as consumers don’t wait for a bill to be ratified!).

Currently, the Hearing Aid Assistance Tax Credit, sponsored by Congressman Jim Ryun (R-KS), has a whopping 42 co-sponsors in the House, and recently Senator Norm Coleman (R-MN) has sponsored the bill in the Senate. The bill has garnered excellent bipartisan support. Although it’s extremely difficult to estimate what the long-term impact of such a bill’s passage would have on the hearing industry, there is almost no doubt that US hearing aid sales—and hearing awareness efforts in general— would experience a radical transformation (for more information, see page 8 of this issue).

Directional hearing aids. In early 2003, less than 29% of all hearing instruments contained directional microphone technology; today, HR estimates that nearly half do. This is another sea-change, perhaps as significant as DSP—it’s just that there aren’t any immediate economic consequences. Directional instruments have been shown to substantially improve hearing in noise and, when properly fitted, increase customer satisfaction.

While there are few guarantees, the hearing care market could find itself in a period of relatively steady growth and excellent prospects for the near-future. w

Karl Strom is editor-in-chief of HR. Correspondence can be addressed to Karl Strom, Hearing Review, 6701 Center Drive West, Ste 450, Los Angeles, CA 90045; email: [email protected].